South Africa going from junk to darling

South Africa’s financial health is showing strong signs of improvement, with the National Treasury on track to post a wider primary surplus than expected in the current financial year.

This shows the National Treasury’s policy of fiscal consolidation is bearing fruit, with expenditure increasing at a slower rate than tax revenue.

However, the country’s stagnant economy poses a major threat to the government’s financial recovery, with fiscal consolidation not enough on its own.

Currently, the economy is growing at a slower rate than the interest rate the government pays on its debt. This means its debt-servicing costs are compounding at a faster rate than the economy, which is unsustainable.

With the National Treasury not having direct control over how fast the economy grows, it can only focus on making government spending more efficient.

It has proven adept at this in recent years, with analysts expecting positive credit ratings adjustments over the next 18 months.

Old Mutual Investment Group portfolio manager John Orford said this would translate into significantly improved investor sentiment towards South Africa and boost economic growth.

Orford explained that the policy of fiscal consolidation is, by nature, quite slow, with results taking years to be seen, as it depends on keeping a tight lid on expenditure and increasing revenue without raising tax rates.

This strategy has resulted in the government running a primary budget surplus for the past two financial years, albeit relatively small surpluses.

These surpluses mean the state is bringing in more through tax revenue than it is spending to provide services and perform its functions. Primary surpluses exclude debt-servicing costs.

This means that, over time, the debt burden should stabilise as new debt issuances slow and then the state can begin paying down its liabilities.

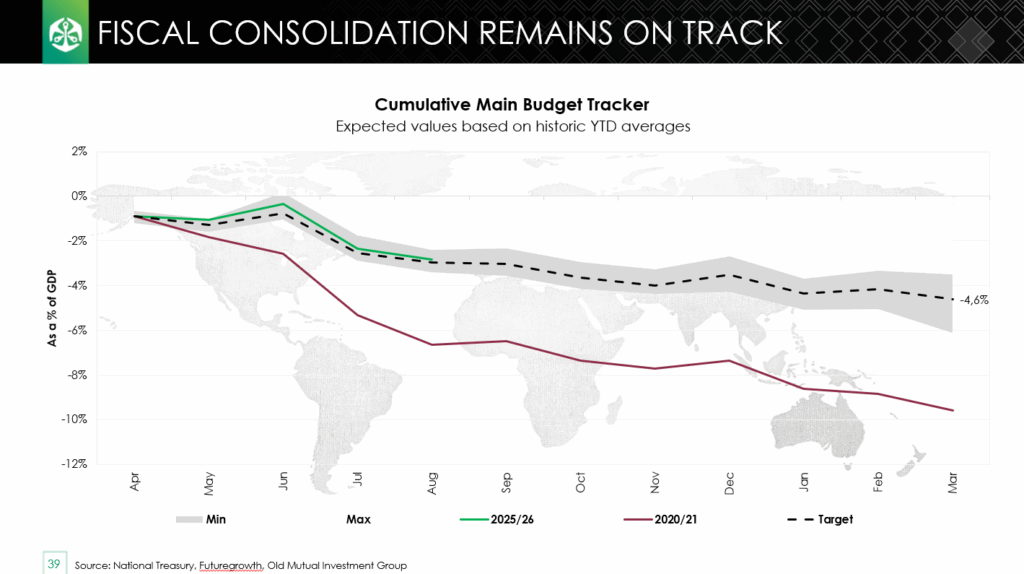

The government is on track to post a wider primary budget surplus in the current financial year than forecasted by Finance Minister Enoch Godongwana in his May Budget Speech.

This is largely due to increased tax revenue from a substantial decline in VAT refunds and relatively slow expenditure growth. Revenue has increased by over 10% year-on-year, while spending growth is at 4%.

Orford said Old Mutual expects a full budget deficit, which includes debt-servicing costs, of 4.6%, which is significantly better than historical readings.

He explained that the outcome may be even better by the end of the financial year, with strong commodity prices likely boosting state revenue further.

The graph below shows the government’s current fiscal account for the financial year and its forecasted target.

Credit rating improvements

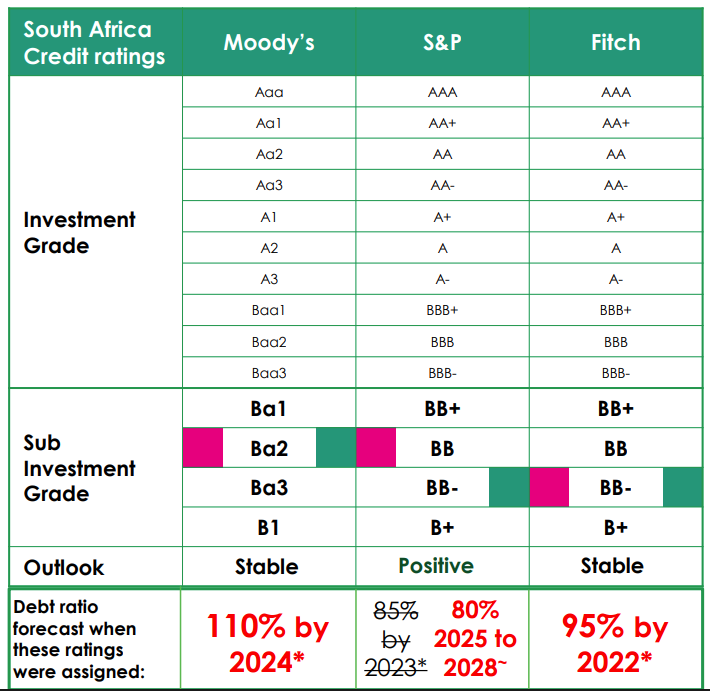

South Africa’s improving financial health is likely to result in improvements to its current junk status credit rating in the coming year.

Currently, South Africa is deep in sub-investment-grade territory with all three major credit ratings agencies – Moody’s, S&P Global Ratings, and Fitch.

The move into junk status was driven by South Africa’s declining financial health, with government spending skyrocketing from 2009 without faster economic growth.

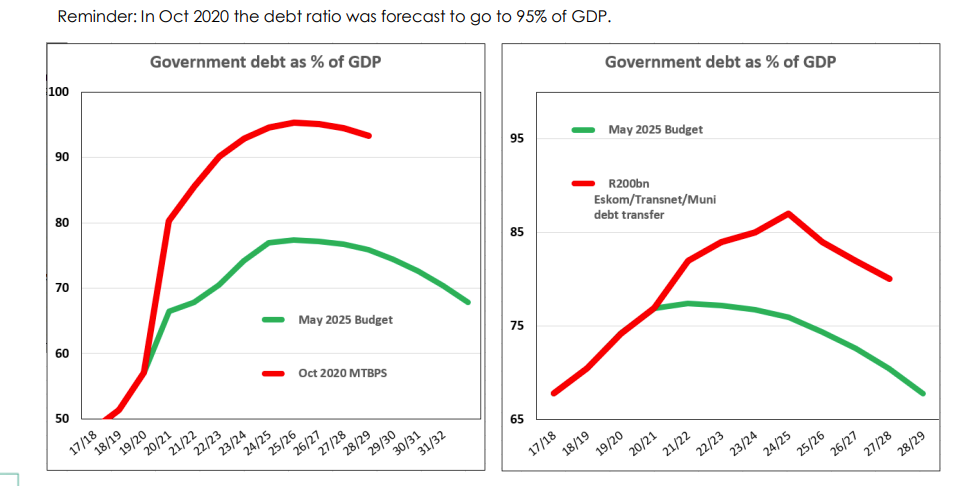

This resulted in consecutive budget deficits and a surging debt burden, which now amounts to over 77% of GDP from just 26% in 2008/09.

As a result, the government is paying over R1 billion a day in interest payments on this debt, crowding out spending in other areas.

Being placed into sub-investment grade prohibits many pension funds and investment schemes from investing in South African assets, as they are considered too risky.

This resulted in significant outflows from local assets in recent years, weakening the rand and limiting economic growth.

Old Mutual chief economist Johann Els explained that this vicious cycle is beginning to flip into a virtuous cycle due to the National Treasury’s implementation of fiscal consolidation.

Coupled with faster economic growth, this could result in a substantial improvement in the state’s finances and thus, improvements in South Africa’s credit ratings.

Els explained that a major reason why South Africa’s credit ratings plummeted was that these agencies simply extrapolated the growth in the country’s debt burden over the past 15 years into the future.

This resulted in forecasts of South Africa’s debt-to-GDP ratio hitting 110% by 2024 according to Moody’s, 80% by 2025 according to S&P and 95% by 202 according to Fitch.

These were the forecasts used when South Africa was assigned junk status. None of these forecasts has materialised in reality.

Els said that this means the ratings agencies are behind the curve, failing to reflect improved growth prospects and declining fiscal risks.

South Africa’s metrics look far better than what was anticipated by the three ratings agencies, pushing Els to say that ratings upgrades could come sooner than some expect.

With improved state finances and enhanced economic growth, improvements in the country’s credit rating could push South Africa into a virtuous cycle.

In this cycle, improvements in the country’s credit rating result in additional investment into the country, accelerating economic growth and further improving the state’s finances, leading to further credit rating improvements.

Comments