South Africa heading for a financial crisis

South Africa’s fiscal accounts continue to deteriorate due to the country’s stagnant economy and upward pressure on government spending.

These two factors have created a vicious feedback loop for the National Treasury, with limited tax revenue growth being coupled with demand for elevated state spending.

Over the past fifteen years, this has translated into skyrocketing state debt and rising interest payments to service these liabilities.

This debt burden, now at over 76% as a share of GDP, is becoming unsustainable, as the local economy will soon be unable to service it.

The interest rate the state pays on its debt is greater than the country’s nominal GDP growth, meaning that the debt-servicing costs are compounding at a faster rate than the economy.

This is not even the full picture, with South Africa’s finances being in a worse position than what is reported, Efficient Group chief economist Dawie Roodt said.

Speaking at the second BizNews Investment Conference, Roodt said the headline debt-to-GDP figure excludes the debt owed by state-owned enterprises (SOEs) and other spheres of government.

“If we want to really compare the finances of the state over time, we have to include the state-owned enterprises and parastatals with the local authorities,” Roodt said.

“For instance, the debt-to-GDP ratio at a national level is just below 77%. But, the actual number, including SOEs and local authorities, is around 85% and it is growing.”

Roodt said that debt is rising as a share of GDP by around two to three per cent a year, which will soon put South Africa in serious financial trouble.

“The national accounts are in a dire state. We are heading for serious financial trouble in South Africa. We are heading for a financial crisis in South Africa,” Roodt said.

The country has limited options to get out of this spiral, with it requiring a combination of fiscal discipline and faster economic growth.

Tax revenue broadly grows in line with GDP growth, unless there are substantial increases in the tax rates, which means that a stagnant economy results in flat government revenue.

Coupled with the pressure to increase state spending to prop up SOEs and municipalities, Roodt said that it looks like South Africa’s finances are only heading one way.

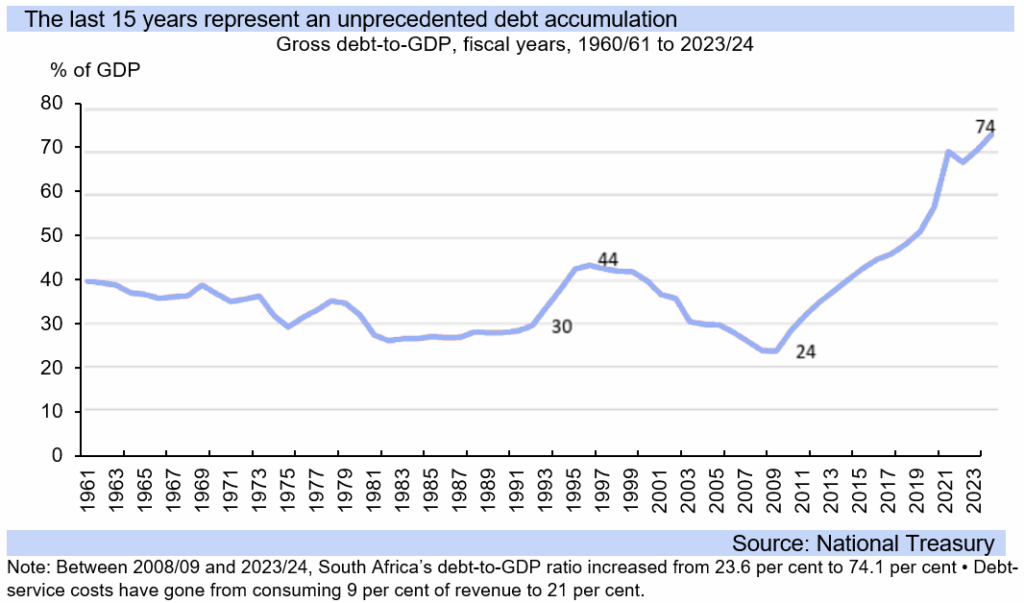

The graph below shows the growth in South Africa’s debt burden over the past sixty years, with the greatest increase occuring since 2009.

Close but no cigar

The National Treasury has repeatedly projected a stabilisation and steady decline in South Africa’s debt burden, only for it to never happen.

Since 2009, almost every budget has projected a stabilisation in the near future, yet the government’s debt has continued to grow.

The last fifteen years are a real exception in South Africa’s financial history, with debt remaining tightly constrained below 45% from 1961 to 2009.

Each postponement of debt stabilisation, while often seeming legitimate at the time, has had a cumulative effect and now puts the country on the edge of a financial crisis.

South Africa’s gross debt has risen from 23.6% as a share of GDP in 2008/2009 to 76.9% at the end of the 2024 financial year.

This escalation has translated into debt-servicing costs surging from 9% of government revenue to 21% and the benchmark bond yield doubling from 6% to above 12% at times.

The deterioration of South Africa’s financial health only accelerated in recent years, with the 2020 lockdowns resulting in government borrowing jumping substantially as economic activity fell.

South Africa has been trying to rein in borrowing and stimulate economic growth for the past decade, without much success.

The National Treasury’s policy of fiscal consolidation has begun to bear fruit, but this will take years before the debt burden is stabilised and reduced.

Importantly, Treasury will maintain a primary surplus in the coming financial year, meaning that tax revenue is projected to exceed non-interest spending.

It will rise over the medium term from 0.7% of GDP to 2.1% in 2027/28. The main budget deficit, which includes interest payments, is expected to continue narrowing over the medium term, reaching 3.2% of GDP by 2027/28.

As a result of running a primary surplus, the debt-to-GDP ratio is projected to peak in the current fiscal year at 77.4% and drift lower over time.

A peak in the debt ratio has been promised for a decade and never happened, but the government is closer than ever due to the consistent running of primary budget surpluses.

Comments