South Africa heading for a serious financial disaster

Despite the National Treasury’s plan to stabilise South Africa’s debt this fiscal year, rating agency Fitch expects government debt to continue rising for at least the next two years.

While doubt accumulation is expected to slow, South Africa’s government debt-to-GDP ratio is projected to reach almost 80% in 2027, putting it well above its peers.

This is largely because state-owned enterprises like Transnet will remain reliant on government support.

On Friday, 12 September, Fitch affirmed South Africa’s Long-Term Foreign-Currency Issuer Default Rating at ‘BB-‘ with a Stable Outlook.

This means South Africa still has an elevated vulnerability to default risk, particularly in the case of unfavourable changes in business or economic conditions.

Fitch explained that South Africa remains stuck at this low rating because of its low real GDP growth, high levels of poverty and inequality, a high and rising government debt-to-GDP ratio, and a rigid fiscal structure that hampers budget deficit reduction.

The government’s immense debt burden has been a major concern for South Africa for over a decade, as the country’s debt remains high and increasing while GDP growth has been slow.

This has placed immense pressure on the national fiscus, as debt servicing costs have increased to the point where the government now spends around R1.2 billion a day.

Debt-servicing costs are the biggest line item in the government’s budget, with the government spending more on interest than education, healthcare and police services.

To address this, the National Treasury plans to achieve a primary budget surplus, which means the government’s revenue outpaces non-interest spending.

Doing this year after year will allow the government to chip away at its debt burden and, particularly when coupled with faster economic growth, stabilise the country’s debt.

Stabilising this debt is crucial for South Africa’s future, as it will allow the government to increase its spending on more productive line items like infrastructure.

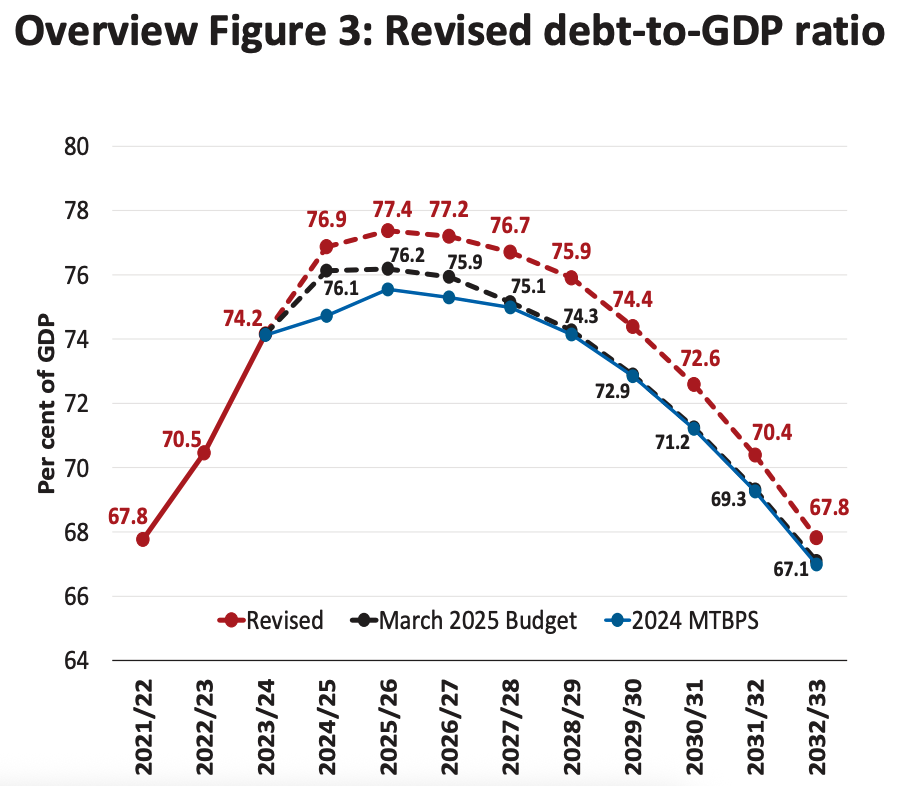

This is the National Treasury’s plan for the 2025/26 financial year, with South Africa’s government debt expected to stabilise at 77.4% of GDP from 78.1% in the 2024 financial year.

However, Fitch projected that South Africa’s debt-to-GDP ratio will continue to grow over the next three years, to 78.5% in FY25, 79% in FY26 and 79.6% in FY27. This will put South Africa far above the 54% 2027 median for countries rated ‘BB’.

The National Treasury’s projections for stabilising South Africa’s debt-to-GDP ratio can be seen in the graph below.

South Africa’s saving grace

While Fitch expects South Africa’s debt to accumulate more slowly over the next few years compared to prior years, it warned that the country’s contingent liabilities remain high.

This is because of the government’s exposure to public institutions like Transnet, independent power producers, and public-private partnerships of R674.9 billion in March 2025.

“We expect contingent liabilities to continue to rise, given state freight transport and logistics company Transnet’s reliance on guarantees from the sovereign,” the agency said.

However, it noted that South Africa also has several factors working in its favour, despite the government’s immense debt burden.

One such factor is the structure of South Africa’s debt. Unlike many of its peers, the country’s debt was mostly raised in rands, with only a small share being foreign currency-denominated.

South Africa’s foreign-currency-denominated debt stands at 10.4% of total debt, far lower than the ‘BB’ median of 55.2%.

This makes South Africa’s debt burden far more stable than many of its peers, as raising debt in foreign currency exposes a country to significant risk, such as foreign exchange rate fluctuations, which often result in the debt burden becoming unsustainable.

In addition, Fitch pointed out that South Africa’s government debt structure has long maturities of over 10 years for total debt.

This means the government will not face frequent rollovers where it must issue new debt to replace maturing bonds. In addition, longer-term debt tends to have more stable interest costs, as interest payments are locked in for longer.

It also makes planning and budgeting easier for the National Treasury and gives investors more confidence that the country is managing its debt prudently rather than relying on short-term borrowing.

While these factors are currently working in South Africa’s favour, it may not be that way for long. The Bureau for Economic Research (BER) has pointed out that South Africa has decreased its rand-denominated debt over the past two years while increasing its foreign currency-denominated debt.

The graph below, courtesy of the BER, shows how South Africa’s reliance on foreign debt to fund its expenditure has grown.

Comments