The companies benefitting from Chinese cars taking over South Africa

South African vehicle and asset financiers are reaping the rewards of the rapid growth of Chinese brands in the country, securing partnerships with them and reaping the benefits of strong sales growth.

Two of the largest players in the market, WesBank and Nedbank MFC, have both pivoted recently from seeing the rise of Chinese brands as a potential threat to an opportunity.

Vehicle lending, particularly for new vehicles, works differently from other kinds of credit extension, which are heavily based on lending to individuals.

In the case of vehicles, it is often done through lending to the dealership and the various financial services companies that operate behind the scenes. This makes it difficult for new entrants to break into the market.

For example, South Africa’s premier digital bank, Discovery Bank, has repeatedly said it has no plans to move into vehicle financing as its behavioural model is centred around individual behaviour, limiting its ability to offer a unique service.

Capitec has moved into vehicle financing but has made a point of lending to individuals directly when they buy used cars rather than trying to break into the new car market.

In contrast to initial fears that the rise of Chinese brands would impact existing relationships and perhaps eat into the market share of existing players, WesBank and Nedbank MFC have continued to grow strongly.

WesBank, in FirstRand’s financial results on 11 September, posted a 20% rise in normalised earnings to R2.38 billion for the past year.

It flagged the rise of Chinese cars in South Africa as a significant opportunity for the division, with it securing partnerships with several brands from the Asian country.

These partnerships are typically through multiple supplier and dealer alliance agreements, which have boosted WesBank’s loan growth.

This is central to WesBank’s operating model, with its focus being heavily on partnering with manufacturers, suppliers, and dealer groups.

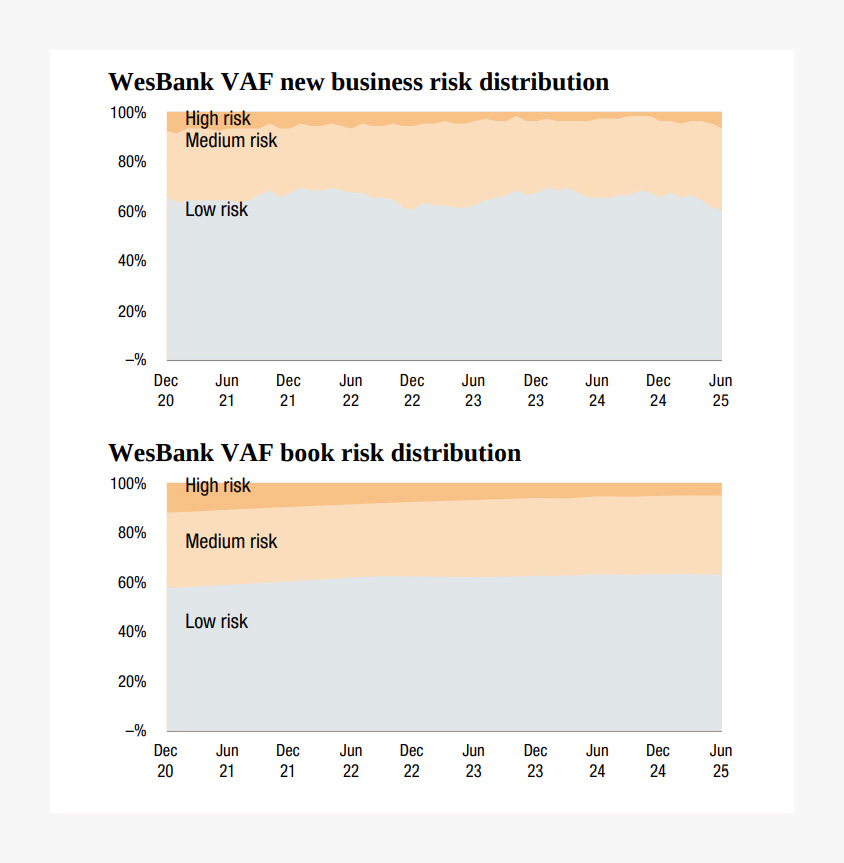

It has shifted in recent years to focus on attracting higher-quality new business, particularly through servicing existing FNB clients.

WesBank noted that competition for new business continues to increase, specifically for these higher-quality clients, which is putting pressure on its margins.

The graphs below show this shift from WesBank towards low-risk clients, with a notable improvement in its risk distribution.

From risk to opportunity

Nedbank MFC is the largest financier of vehicles in South Africa, with its market share growing to 36.2% in the past financial year.

This puts it at the coalface of the shifts in South Africa’s new car market and the rise of used car players such as WeBuyCars.

The bank’s operating division has been aware of the shift towards value over the past few years, with the rise of Suzuki, Chery, and Haval in South Africa.

It previously noted that Chinese cars may face some headwinds in the market from the sheer number of brands, resulting in a cannibalisation of their market share.

Nedbank MFC expects established players to benefit from this until new entrants build out their network and can offer similar levels of service.

Nedbank CFO Mike Davis explained to Daily Investor, following the bank’s interim results earlier this year, that the emergence of Chinese cars and used car players has not significantly impacted its vehicle financing business.

One of the bigger threats to Nedbank MFC has been the rise of used car sales in South Africa, alongside the strong growth of WeBuyCars, due to the affordability of used cars in comparison to new models.

This has also been coupled with a rise in Chinese vehicles, which do not have a pre-existing dealership network or relationship with banks, posing a threat to existing financiers.

“We currently hold a 36% market share in the vehicle financing segment, and we have continued to take market share in the past year,” Davis said.

“We have gotten a lot of questions about new versus used and new Chinese vehicles coming into the market and the impact those trends would have on our financing.”

“To answer those questions, we have grown market share effectively, where we have been comfortable growing our share in vehicle finance.”

This indicates that Nedbank MFC is going from strength to strength, with it being one of the few areas in which the bank managed to grow its lending market share.

Davis said that faster-growing real incomes and lower interest rates will improve the economies of the motor vehicle finance business in the second half of the year.

“We are coming off the tail end of an interest rate hiking cycle from 2021, with prime rates peaking at 11.7%%,” he said.

“We have seen rates be cut by 50 basis points in 2024, followed by 75 basis points in 2025. Typically, it would take 18 months before this translates into a positive impact on impairments.”

“So, we should see the economics of that business improve in the second half of the year through a lower bad debt impairment number.”

Comments