Make or break for South Africa

South Africa is at an inflexion point in its journey towards energy security, with the country needing to invest heavily in new generation capacity or risk being plunged into a new wave of load-shedding in the coming decade.

Simultaneously, the public and private sectors will need to invest billions to upgrade the country’s grid, ensuring that new projects can contribute meaningful generation capacity.

The key to avoiding disaster is reforming the electricity sector, opening it up to increased competition and private investment in infrastructure.

These reforms need to be accelerated to enable billions from the private sector to flow into electricity generation and transmission over the coming decade.

This is feedback from Nedbank’s Corporate and Investment Banking (CIB) division, which outlined South Africa’s electricity challenges in a recent report on the country’s energy prospects.

“South Africa is at a critical juncture in its energy journey. The decisions made today will have long-lasting impacts on the nation’s growth and environmental protection,” the managing executive for Nedbank CIB, Anél Bosman, said.

The country’s electricity supply crisis has seen significant improvements, with Eskom’s performance stabilising and new generation coming online from the private sector.

Crucially, structural and commercial changes initiated by the crisis are driving ongoing reforms in the sector, which promise to boost investment and energy security.

“The crisis has redefined the relationships between the state, Eskom, transmission system operators, consumers, and the private sector,” the report read.

After 262 days of load shedding in 2023, the situation improved in 2024, with no power cuts for two consecutive quarters.

Eskom invested heavily in maintenance, improving the energy availability factor of its plants from 57% to 67% by July 2024. This is still far below the 75% target set by the 2019 Integrated Resource Plan (IRP).

This was coupled with lower demand and increased self-generation from rooftop solar installed by households and businesses.

Small-scale embedded generation (SSEG) registrations increased by 474% and solar PV installations by 138% between December 2022 and December 2024.

As a consequence, the utility-scale, distributed, and SSEG installed capacity increased from less than 2 GW to just under 10 GW over the period. Rooftop solar installations increased from about 2.5 GW to about 6 GW

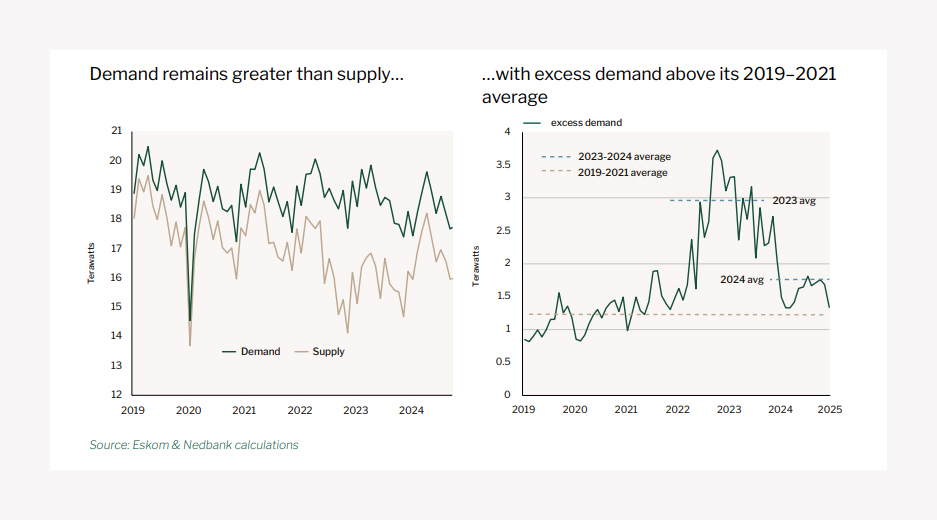

Despite these improvements, the electricity supply remains unstable due to constrained capacity, with excess demand being managed through load reductions, imports, and the use of expensive open-cycle gas turbines (OCGTs).

Nedbank stated that the lack of grid capacity, particularly in the Cape provinces, poses a threat to the integration of new projects that could secure South Africa’s energy future.

The graph below illustrates that demand in South Africa consistently exceeds supply, with excess demand surpassing the average of 2019-2021.

New generation capacity will not be enough

South Africa is at a critical phase in its long-term energy transition plans, facing a looming crisis of demand significantly outstripping supply.

Despite the increased investment in new generation capacity and planned investments, it is unlikely to be enough for South Africa’s future needs.

Demand still outstrips supply by a significant margin in South Africa during peak hours and is expected to increase further as the population grows and economic activity expands.

Currently, economic growth is still limited by the country’s insufficient electricity supply, with any pickup in activity being capped by an energy shortage.

This problem will become far more acute over the next decade, when Eskom must begin decommissioning some of its coal-fired power plants.

A report from Cresco and Standard Bank’s CIB division showed that while load-shedding has been significantly reduced since March 2024, the country’s long-term energy security now depends on getting new capacity quickly.

New capacity is needed from various forms, including renewables, gas, storage, and potentially nuclear in the long run.

The report highlighted that the IRP 2024’s most significant shift is the Cabinet’s decision to keep Camden, Grootvlei and Hendrina power stations running until 2030.

While the extension of the life of these coal-fired power plants gives South Africa additional time and flexibility to address its energy shortfalls, it does not appear to be enough.

“Considering the looming risk of another energy crisis, which may materialise as soon as coal decommissioning is resumed, new capacity additions and RE implementation need to increase at a dramatic rate,” the report read.

“There is no room for error in REIPPPP Bid Window 7, gas-fuelled generation capacity additions or delays in the private sector procurement.”

The graph below illustrates the projected distribution of energy generation across a 24-hour day in 2040, based on currently planned and announced projects.

It indicates that there will still be substantial shortfalls in energy supply during significant parts of the day, requiring ‘top-ups’ with gas, nuclear, or other types of generation.

The Just Energy Transition Partnership is a noble and essential effort, but total generation still needs to meet demand, both annually and hourly, the report said.

Comments