South Africa’s saving grace is right beneath its feet

Despite being a net importer of oil and refined products, South Africa is set to avoid the worst consequences of the fallout from the war in Iran.

The conflict has pushed oil prices to above $100 per barrel amid disrupted supply, and the rand to around R17 against the US dollar as investors search for safety.

This has severe consequences for fuel prices in South Africa, with petrol and diesel set to rise by the largest amounts in history.

The greater concern for many is that this will give South Africa an inflationary shock and potentially prompt the Reserve Bank to hike interest rates, slowing consumer spending and economic growth.

These effects appear significant, with FNB CEO Harry Kellan warning that the fallout from the conflict in Iran may derail South Africa’s steadily improving economic fundamentals.

However, Symmetry chief investment strategist Izak Odendaal explained that South Africa is set to avoid the worst consequences of the war due to a much-maligned resource beneath the country’s soil – coal.

While South Africa is a net importer of oil and refined petroleum products, it is not a net energy importer. This distinction is vital.

Electricity is by far a larger source of energy than oil-based fuels in South Africa, accounting for a bigger share of the consumer price index (CPI) and serving as a larger input into the economy.

South Africa produces its own electricity from resources it has abundant supplies of, mainly in the form of coal-fired power plants and increasing renewable energy.

The country also exports a lot of coal, which has seen an increase in price amid the energy shock from the Middle East. This will boost South Africa’s balance of payments and support the rand somewhat.

While the impact of the war in Iran will be severe on South Africa with regard to fuel prices, inflation and interest rates, the country is getting off relatively lightly compared to others.

Countries that are hit the hardest are those that are net energy importers and reliant on fossil fuels sourced elsewhere to keep the lights on.

This exposes them much more significantly to the conflict in the Middle East as energy imports effectively power their entire economies. This is not the case in South Africa.

The storm is coming

South Africa may be somewhat insulated from the worst effects of the conflict in Iran, but it will still feel the pain from disrupted international oil supplies.

The disruption has sent oil prices skyrocketing and the rand weakening, setting South African motorists and transporters up for record pain at the pumps in April.

This is not the Reserve Bank’s chief concern, as fuel prices account for only 3.8% of the CPI.

However, it is still enough to push headline inflation out of the Reserve Bank’s one percentage point tolerance band around its 3% target.

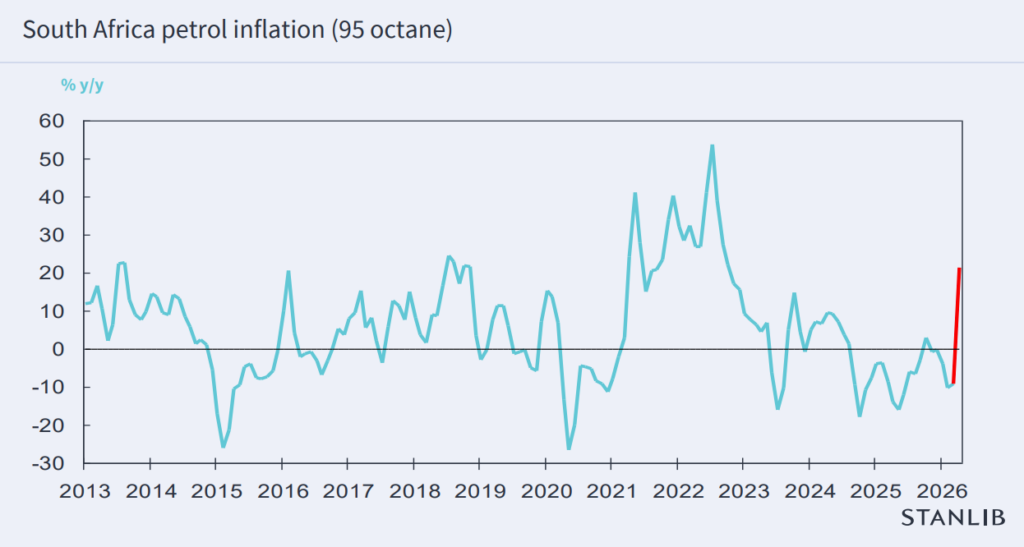

Odendaal estimated that fuel price inflation will accelerate to around 16% in April, once the R4.80 per litre petrol price hike is reflected.

Fuel’s direct weight in the CPI basket is only 3.8%, meaning that it will directly add between 0.6 and 1 percentage point to headline inflation in April, if current price hikes hold.

The Reserve Bank’s eyes will be on the second-round effects of rising fuel prices, with it watching to see if it translates into rising prices for other goods and services.

If these prices rise, it indicates that inflation is becoming entrenched in South Africa and will be sustained for a prolonged period. This situation is one the Reserve Bank wants to avoid.

Central banks also have little impact on supply-side inflation as they cannot drill for oil or open the Strait of Hormuz. They can only lower the demand for fuel.

This limits the impact of interest rate hikes on taming supply-side inflation. Where interest rate hikes have a significant impact is on other prices in the economy, as they will reduce demand for products and services.

Another factor at play in the Reserve Bank’s calculations is that a fuel price shock will be temporary, and so it will not want to put the brakes on economic growth for an event that will not be repeated.

Stanlib chief economist Kevin Lings has analysed the history of fuel price inflation in South Africa. This research showed that it is very rarely contained and stable.

For the majority of the time over the past two decades, fuel prices have either been increasing or decreasing at a rate greater than 10% year-on-year.

This means that fuel prices are highly volatile, with a sharp increase likely to be followed by a sharp decrease, meaning the Reserve Bank will try to look beyond fuel prices for signs of more sustained price increases in the economy.

Comments