Johann Rupert’s historic company faces a big challenge

Johann Rupert’s Remgro continues to trade at a significant discount to its net asset value (NAV), despite efforts from its management team to unlock value for shareholders.

While this presents a problem for the company, it also presents a substantial opportunity for investors who can invest in the company at a relatively cheap price to NAV.

Furthermore, this discount is likely to narrow to its long-term average, indicating a large potential for upside in the share.

Allan Gray is one of the large asset managers exposed to Remgro through its clients’ portfolios, with analysts from the firm explaining their reasons for investing in South Africa’s premier investment holding company.

Jonty Fish and Malwande Nkonyane explained in a recent research note that it is not unusual for holding companies to trade at a discount to the sum of their underlying investments.

Typically, the reason for this discount is additional tax obligations, head office costs, management and performance fees, or a lack of disclosure in investee companies.

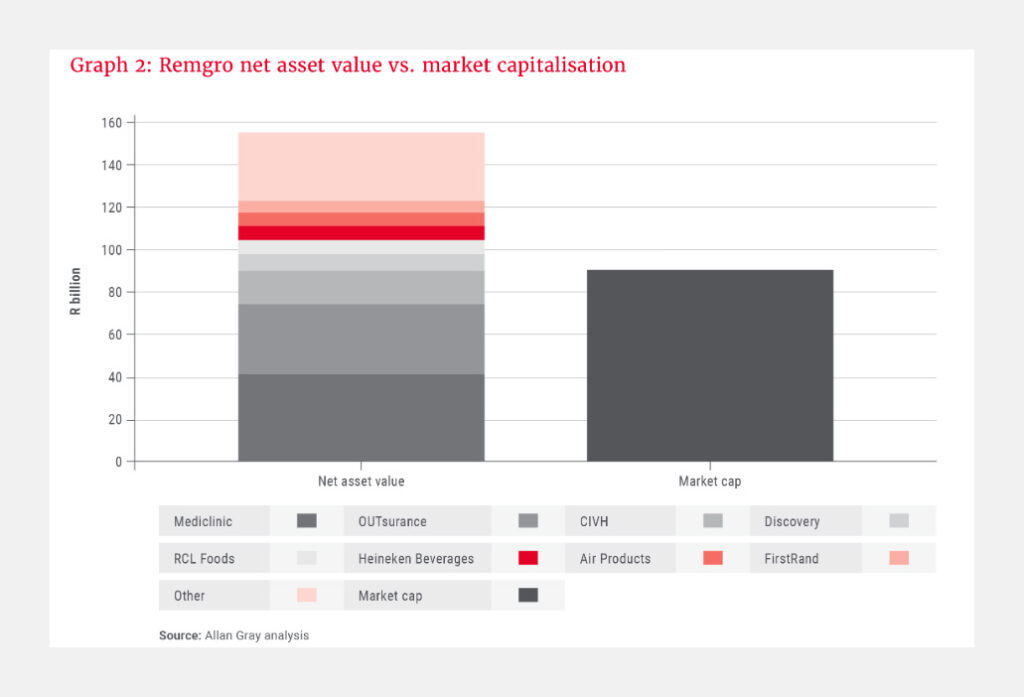

Remgro has historically traded at an average discount to its NAV of around 20%, with some periods seeing this dip below 10% and recent extremes reaching close to 50%.

At the end of October, Remgro was trading at a discount to its NAV of close to 40% – well above the long-term average.

Fish and Nkonyane pointed to some operational headaches as the reason for this wider discount in recent months, alongside a wait-and-see approach by investors to large deals involving Remgro.

The delayed deal between Vodacom and Maziv, which is controlled by Remgro’s Community Investment Ventures Holdings (CIVH), was a major reason for investor hesitation.

Operationally, integration issues at Heineken Beverages and earnings pressure at Mediclinic Switzerland have soured investor sentiment.

“Despite acknowledging that some of the market’s concerns are valid, we think prevailing pessimism is overdone, especially since quantifiable reasons for the discount (tax and head office cost) justify a discount less than 10%,” the analysts said.

To put the discount into context, Fish and Nkonyane said that the current market capitalisation only represents Remgro’s stake in OUTsurance, 75% of its Mediclinic stake, the company’s share in CIVH, and its cash.

In other words, Fish and Nkonyane believe that the market is placing a nil value on a large portion of Remgro’s investments.

From tobacco to titan

Remgro has undergone an immense transformation in its 80-year history, with the company going from a small tobacco player to a blue-chip JSE-listed giant.

The company’s history dates back to the 1940s, when founder Dr Anton Rupert established a tobacco company that would become Rembrandt.

It grew rapidly within the tobacco industry, consolidating its holdings with Rothmans International and later merging those interests with British American Tobacco (BAT).

Rembrandt also dipped its toes into other sectors, such as wine and spirits, financial services, mining, printing and packaging, medical services, engineering and food processing.

Its largest transformation would come in the 2000s, when Rembrandt was restructured to form two companies – Remgro and VenFin.

Remgro would house the tobacco, financial services, mining, and industrial businesses, while VenFin would control the telecommunications and technology interests.

In 2008, Remgro unbundled its BAT stake, marking the end of an era. Until then, the company had largely remained a tobacco play.

Today, Remgro is a diversified investment holding company with over 20 underlying investee companies that straddle the South African economy.

If you drink Heineken beer, Savanna or Amarula, use Flora margarine, eat Yum Yum peanut butter, are insured by OUTsurance or Discovery, bank with FNB, or have visited a loved one at a Mediclinic hospital, you have interacted with one of Remgro’s many investee companies.

Less familiar to ordinary South Africans are Remgro’s industrial assets, such as Air Products South Africa, which manufactures and distributes speciality gas products.

This company is one of the best-performing in recent years, growing its topline at a rate greater than 10% per annum for the past decade.

Fish and Nkonyane explained that as more of these stories come to light and management continues executing on its plan to unlock value, the discount should narrow.

They outlined several key developments in recent months –

- The recent approval of the Vodacom/Maziv deal with updated terms valuing Maziv at a large premium to management’s value.

- Heineken Beverages is overcoming its integration issues, allowing the business to focus on reigniting growth.

- Good execution of cost control initiatives at Mediclinic Switzerland, combined with lower Swiss interest rates, should be a tailwind for earnings.

- Unbundlings and restructurings which have unlocked value for shareholders. Over the last few years, investment holding company RMH, logistics company Grindrod and, more recently, eMedia Holdings have been unbundled. Rand Merchant Investment Holdings’ structure was simplified, which led to serious value unlock for shareholders in relation to the direct OUTsurance listing. RCL Foods also sold Vector Logistics and unbundled Rainbow Chicken.

These initiatives highlight Remgro management’s focus on unlocking the discount and creating value for shareholders, the analysts said.

Comments