The company that bet against the South African government – and won

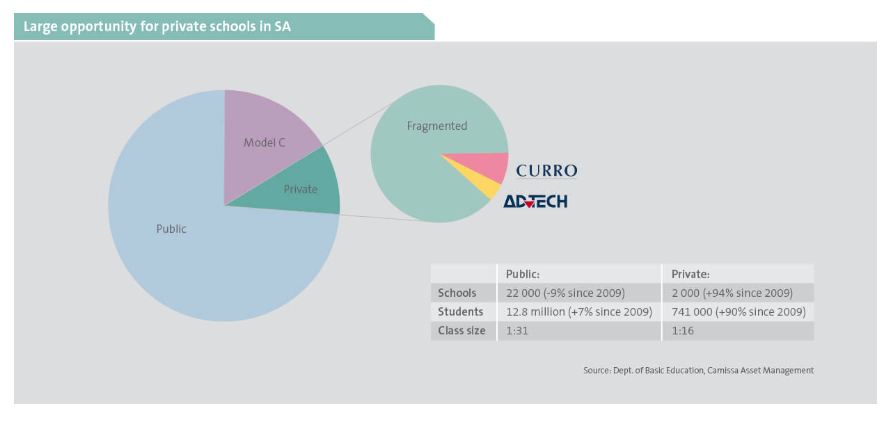

Private schools continue to grow rapidly in South Africa, with the total number doubling in the past 15 years, as public education steadily collapses across the country.

This has left these private schools playing an increasingly important role in addressing the challenges of declining academic outcomes in South Africa, while opening up a significant opportunity for them to benefit financially.

Private schools have also become the preferred choice for parents due to their smaller class sizes, modern facilities, and more personalised learning experiences.

One such company is Curro, which is the largest private school group in South Africa, serving affordable, high-quality education to a broad cross-section of South African society.

The company’s rapid growth and financial success were outlined by Camissa Asset Management investment analyst Edward Mtsweni.

Mtsweni explained that Curro has benefitted immensely from the decline of public education in South Africa, with thousands of learners shifting to private alternatives due to poor academic outcomes in the public sector.

While the vast majority of students are still educated in the public sector, private schools have grown rapidly over the past 15 years.

Since 2009, there has been a 10% decline in the number of public schools in South Africa, while private schools has nearly doubled.

Private schools now educate 741,000 students in South Africa, with an average class size of 16 pupils. The public sector educates 12.8 million students at a class size of 31 pupils.

Curro’s business model is built on a steady stream of school fee income, providing predictable cash flow throughout the academic year.

This is buoyed by ancillary income from facility rentals, uniform sales, catering services, aftercare and boarding facilities.

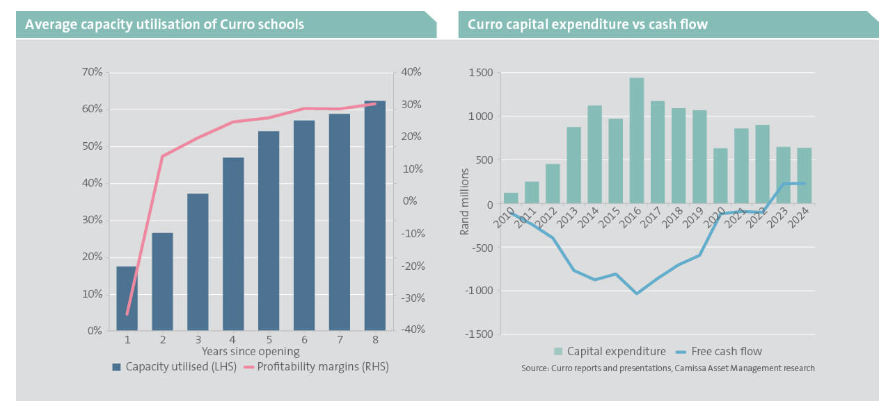

Mtsweni explained that opening a school is not an easy task, with it requiring substantial investment and significant upfront costs in the form of building infrastructure and hiring staff.

These two elements make up 70% of the total cost of operating a school and are baked in before learners are enrolled.

As a result, schools tend to operate at a loss for the first few years of operation, with a steady intake of new learners required to boost fee income and the overall financial performance.

A new Curro campus typically takes three to five years to reach profitability. However, once the cost-coverage threshold is reached, additional learners can be added at minimal incremental cost.

This results in income growing much faster than expenses, creating a profitable business with a highly predictable financial performance.

The rapid growth of private schools and the profitability dynamic can be seen in the graphs below.

Curro goes from challenger to champion

Established in 1998, Curro has grown strongly over the past two decades to have more than 180 schools in operation across South Africa.

While private schools are typically associated with high fees and exclusivity, Curro has broken this by implementing a tiered pricing model.

This enables it to deliver private education to a broader segment of the population, making it a competitive alternative to both public schools and traditional private players.

Curro’s tiered schooling model can be seen below, ranging from lower-income options up to select schools that compete with traditional private schools.

- Meridian Schools: Curro’s most affordable model is developed in partnership with the PIC and Old Mutual. These English-medium schools serve lower-income urban communities and follow the South African NSC curriculum.

- Academy Schools: Located in urban areas and aimed at lower- to middle-income families, these English-medium schools also follow the NSC curriculum.

- Curro Schools: The group’s core model serves middle- to upper-income families. These co-educational schools offer grades R to 12, often including preschool phases. They follow the South African Independent Examination Board (IEB) curriculum.

- Select Schools: These well-established schools are acquired by Curro and maintain their original identity while benefiting from Curro’s support. They are English-medium and offer the IEB or Cambridge curricula.

While this tiered approach and Curro’s business model enable the company to rapidly grow its footprint, it has come with the problem that a considerable number of its schools remain below optimal learner capacity.

This means they are not as profitable as they can be and do not benefit from the positive dynamics where more students can be added with minimal additional cost.

As a result, Mtsweni said schools operating below breakeven levels have significantly weighed on Curro’s financial performance in recent years.

This has forced the company to shift its approach from rapidly growing its footprint to prioritising filling existing capacity at its schools.

This shift should result in improved operational efficiency and better returns on invested capital, as less expenditure will be required to build out new infrastructure.

With much of the physical infrastructure already in place, Curro is well-placed to generate more cash from operations as it fills up capacity, allowing for debt reduction and improving shareholder returns.

The transition from high-growth, capital-intensive expansion to a more cash-generative phase will be central to shaping the group’s future value creation.

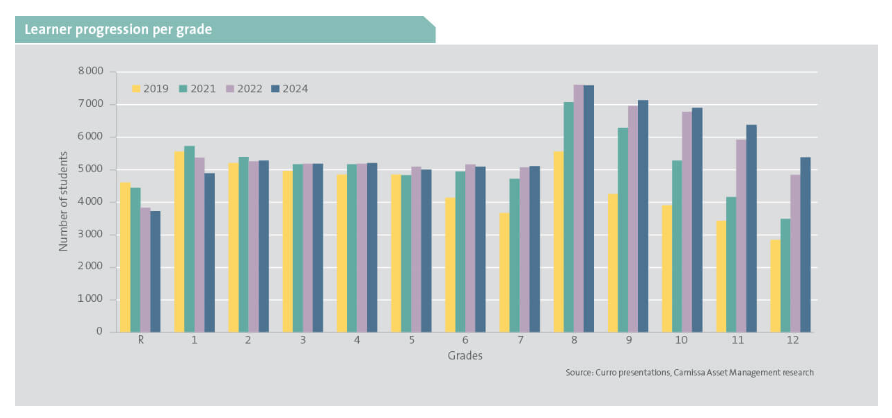

Curro has also struggled with passing on rising costs to parents, which has seen learners decline at some of its schools. This has particularly impacted enrolment numbers in lower grades.

The company has also struggled with campus development, with some cases resulting in schools being built in areas with weak underlying demand and a lack of affordability.

Less-than-ideal locations have therefore made it difficult to achieve the necessary scale for profitability, leading to underutilised capacity, elevated cost structures and a select group of underperforming Curro schools.

Mtsweni believes these issues are largely manageable and can be addressed with a few interventions and a change in strategy.

The graph below shows Curro’s learner progression per grade, indicating the impact of pricing pressures in lower grades.

Going private

Curro is now set to enter a new chapter, with billionaire Jannie Mounton planning to buy the education group through his foundation.

At the end of August 2025, the Jannie Mouton Foundation offered to acquire all of Curro’s shares of around R7.2 billion and make it a non-profit.

Mouton is one of South Africa’s most successful businessmen and founded the PSG Group, which has had a hand in some of the country’s best businesses, including Capitec, PSG Financial Services, Curro, and Stadio.

The foundation said it aims to make a meaningful contribution towards improving South Africa for all its people and ensure it remains the preferred place to live in and raise children for generations to come.

“Education has always been close to Jannie’s heart; he sees it as a powerful way to uplift communities in South Africa and help South Africans reach their full potential,” it said.

“That’s why the trust is putting almost all of its resources into making this happen. By working with Curro, the trust believes it can create far greater impact.”

This impact could take the form of expanding bursary opportunities and developing educational infrastructure in areas often overlooked by profit-driven institutions.

“Building and improving schools takes time, and most investors aren’t willing to wait that long. But the Trust is in it for the long haul, focused on making a real, lasting difference,” it said.

“For the Jannie Mouton Foundation, acquiring Curro represents a game-changing R7.2 billion donation in quality education – quite possibly the largest philanthropic contribution South Africa has ever seen,” Jan Mouton said.

“Over time, this will open the door for thousands more children to attend Curro schools through bursaries, broadening access to excellent education.”

“At the same time, Curro shareholders stand to benefit from a 60% premium on the current market price, ensuring that both education and investors gain from this bold initiative.”

Comments