The ‘mismatch’ costing South Africa R50 billion a year

The mismatch between South Africa’s economic fundamentals and its credit ratings costs the country around R50 billion a year in additional debt-servicing costs.

South Africa’s economic and financial fundamentals are better than the country’s credit rating indicates, resutling in it paying an excessive premium on its debt.

This is feedback from Standard Bank CEO Sim Tshabalala, who outlined the mismatch and the cost it has on the country and financial institutions.

Tshabalala told Daily Investor that the bank has engaged with rating agencies on this mismatch and the severe impact it has on the country.

“I would invite you to analyse the economic and financial fundamentals of South Africa and compare them relative to the country’s credit rating,” Tshabalala said.

“I would contend to you that you will find there is a mismatch between those fundamentals and the ratings. Put differently, our research at Standard Bank shows that South Africa should not be BB-, it should have a BBB rating.”

This results in a misconception about South Africa’s economic and financial stability, forcing it to pay an excessive premium on its debt.

While South Africa’s economy is not growing, it has a relatively stable macroeconomic environment and a highly sophisticated financial system.

These characteristics are unique among its peers and are vastly different to other countries that are rated as BB- by credit rating agencies.

“This results in an excessive premium that is being paid on its debt. It is a result of that mismatch between the fundamentals and ratings that South Africa is paying R50 billion more in interest costs than it should be,” Tshabalala said.

The R50 billion going to additional interest payments could be used much more effectively to fund education, healthcare, or infrastructure development.

“The additional cost is why it is so important to keep the debate alive and keep making the argument. It is not a trivial matter,” he said.

“We are in the process of engaging the rating agencies as we speak. We are going to keep making this point. Just look at the fundamentals and your rating. The mismatch is too large for us not to have a say.”

Rating agencies are behind the curve

South Africa’s deteriorating credit rating over the past decade coincided with slowing economic growth and increased government spending.

As a result of that combination, the government’s debt burden has ballooned to over 76% as a share of GDP, and it costs R1 billion a day to service.

Being placed into junk status prohibits many global pension funds and investment schemes from investing in South African assets, as they are considered ‘below investment grade’.

This resulted in significant outflows from South African assets over the past few years, significantly weakening the rand and further limiting economic growth.

In turn, this creates a vicious cycle where declining investment further weakens economic growth, negatively impacting the government’s finances and increasing the risk of investing in the country.

South Africa has been in this cycle for the past 15 years, with the government running its last budget surplus in the 2007/08 financial year. Since then, it has consistently run deficits while economic growth has slowed.

However, things are now looking up for the country, with its economic growth outlook improving and state finances stabilising.

The National Treasury’s policy of fiscal consolidation, effectively keeping spending growth at or below inflation, has begun to bear fruit.

As a result, the government has managed to record successive primary budget surpluses, which are expected to widen in the coming years.

A primary budget surplus means the government is spending less than it earns from tax revenue, allowing it to limit the growth in debt.

As a result, the government’s debt burden is expected to peak in the coming financial year and begin to trend downward as funds are freed up to start paying down the principal owed.

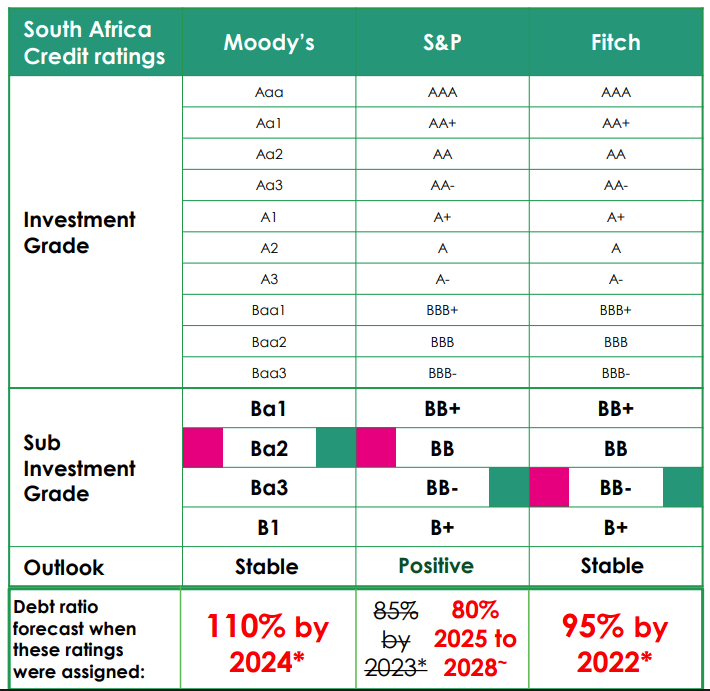

Old Mutual chief economist Johann Els said the combination of these two factors shows that credit rating agencies are behind the curve on South Africa.

When these institutions downgraded South Africa to its current ratings level, they forecasted a significantly higher debt-to-GDP ratio for the country.

This was essentially an extrapolation based on the government’s accelerating spending in the 2010s, which was coupled with poor economic growth.

These metrics look far better than what was anticipated by the three ratings agencies when they assigned South Africa’s latest ratings.

Moody’s anticipated the debt-to-GDP ratio would hit 110% by 2024, S&P saw it reaching 80% after 2025, and Fitch forecast it hitting 95% by 2022.

South Africa’s finances are in a far better position at the end of the 2024 financial year than any of those forecasts, pushing Els to say that they are behind the curve.

This can be seen in the table below, courtesy of Els. South Africa’s debt-to-GDP ratio is at 76% and is expected to stabilise below 80%.

Comments