South African consumers in deep trouble

South African consumers are still under immense financial pressure, with spending growth slowing despite a sharp decline in inflation and interest rates beginning to come down.

Consumers are also looking beyond credit and loans for additional cash to spend, with many tapping their retirement savings under the new two-pot system.

This is feedback from Discovery Bank and Visa, which outlined South Africans’ spending behaviour in their third SpendTrend report.

Discovery Bank CEO Hylton Kallner said the report is the most comprehensive analysis of spending in South Africa, drawing on data from over 2.6 billion transactions.

The bank uses the data it collects from its client base alongside Visa’s data to compile the report while also taking a survey of 1,000 South Africans across different banks and income segments.

Kallner explained that the aim is to determine how much South Africans spend, what they spend on, and how they spend their money.

The bank then uses this data to inform the new products and services it develops and improve its existing product set.

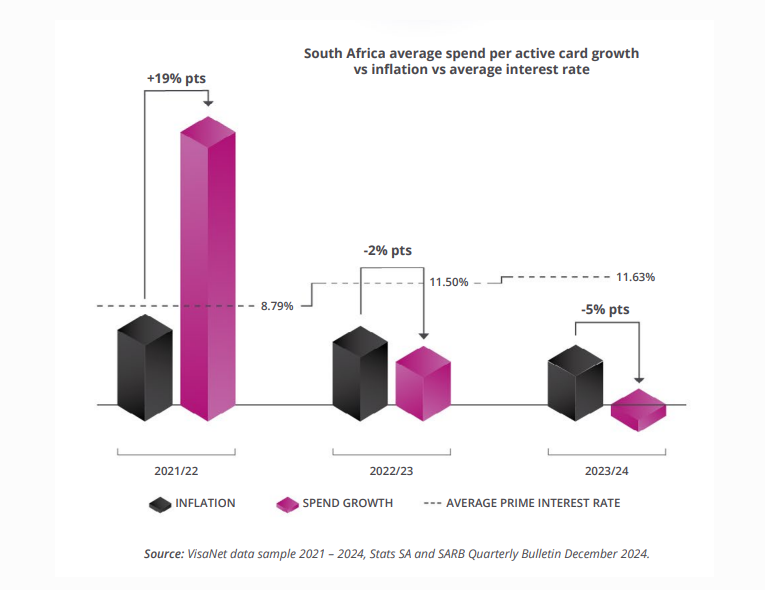

The key trend flagged in the report is that consumer spending is coming under renewed pressure in South Africa despite a decline in inflation.

Kallner explained that average spending per card is flat year-on-year and trended downwards throughout 2024. The growth in spending was below the headline inflation, with consumers spending less in real terms.

Consumers continued to hunt for value in South Africa, drawing back on discretionary spending on travel and entertainment.

These drawbacks were also used to fund increased fuel expenditure as South Africans returned to the office.

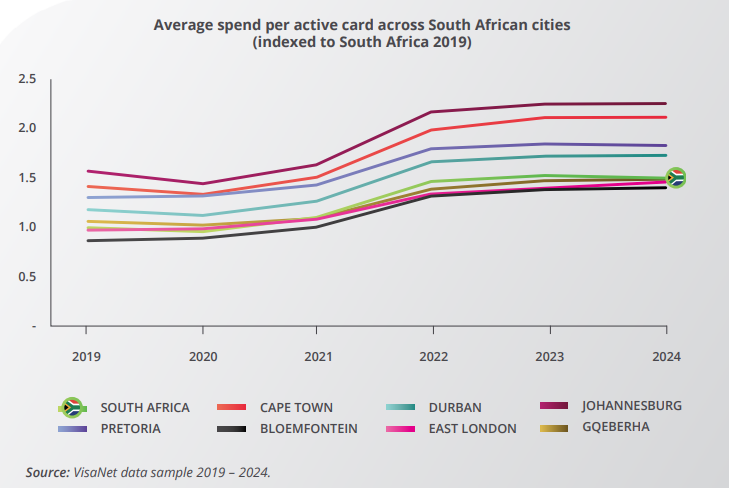

The report also draws on data from South Africa’s major metros – Joburg, Cape Town, Durban, and Pretoria – to understand local spending habits.

This data is then compared to select secondary cities – East London, Gqeberha, and Bloemfontein – which were added to the report for the first time this year.

The data showed that spending in these secondary cities grew faster than the larger metros in 2024 as the individuals living there experienced slightly less financial pressure.

This can be seen in the graphs below, which compare spending across South Africa’s cities alongside the decline in real consumer spending.

How South Africans are coping

Kallner explained that South Africans are increasingly turning to credit and retirement savings to supplement their disposable income, reflecting the immense pressure consumers are under.

The number of credit cards in use across South Africa has increased by 53% since 2020, and demand for loans remains strong.

While more cards are being issued and average new credit limits have increased, overall spending per active card has remained steady.

This suggests that consumers are distributing their spending across multiple payment methods rather than significantly increasing their credit card usage.

The shift means credit card numbers are growing faster than total spending, leading to lower average spending per card.

This also means that consumers are using multiple credit cards to tap extra sources of credit and that people are optimising rewards and benefits by strategically using different cards.

The bank’s consumer survey with Visa revealed that 84% of South Africans prioritise rewards and cash back when spending.

This is supported by spending data, which showed that consumers tend to spend more at loyalty partners than elsewhere.

Over 80% of South Africans now engage more with their credit card rewards and benefits than they did a year ago.

Another way in which South Africans have been supplementing their income to support spending is by tapping into their retirement savings under the new two-pot system.

By the end of 2024, when the system had only been implemented for four months, over 1.9 million withdrawals had been processed through SARS and over R35 billion withdrawn.

Comments