Big changes for how credit cards are used in South Africa

Young South Africans are increasingly using credit cards for everyday spending, rather than emergencies or large purchases.

This marks a dramatic shift away from how credit cards have been historically used by previous generations and their relationship with debt.

Standard Bank revealed this shift in its 2026 Youth Barometer, which is a research paper based on data from its personal banking clients between the ages of 18 and 35.

The bank collects this data and produces reports to better understand how young individuals are engaging with its products and how services can be adapted to their needs.

In its second year, the barometer focuses on the spending habits of young South Africans alongside their relationship with insurance and investing.

Head of personal banking at Standard Bank South Africa, Tshiamo Molanda, explained that the finances of young South Africans are increasingly complex compared to previous generations.

While they retain the traditional goals of home and vehicle ownership, they face a much more difficult path in reaching them.

This is primarily for greater participation in the economy, with the youth looking to use property as a means of building wealth and buying cars to expand their job opportunities.

“For previous generations, adulthood followed more predictable pathways. Education led to employment, which led to financial stability,” Molanda explained.

“While these outcomes remain highly desirable, the pathways towards them have become increasingly fragmented, competitive, and financially demanding.”

This means that “doing everything right” no longer guarantees expected outcomes, while they may improve opportunities, uncertainty remains constant.

“Young people are entering adulthood within an environment where pathways towards stability have become increasingly complex and less linear,” Molanda said.

“For many, instability has not been experienced as a temporary period, but rather as an ongoing condition shaping expectations, behaviours, and perceptions of the future.”

This has been driven by young people growing up amid elevated economic uncertainty, rising living costs, technological change, disruption, and increased social complexity.

Overall, this fundamentally changes how young South Africans engage with financial products and what they use them for.

Credit cards on the rise

The area where different financial behaviour is the clearest is that of credit and lending, with the youth of today being much more willing to engage with these products.

Having grown up in households with credit cards, personal loans, or revolving credit, young people are far less fearful of taking on debt.

This does not mean they are reckless with credit or debt, but rather that they use it in a different manner and more frequently.

Head of credit card at Standard Bank South Africa, Tumelo Ramugondo, explained that historically, credit was used for emergencies or large payments.

South Africans of old would use credit cards or personal loans to cover a trip to the hospital or purchase a TV and other appliances. This would then be steadily paid off over a period of time.

In contrast, young South Africans nowadays use credit cards for everyday spending instead. These cards are also typically their first exposure to debt.

Ramugondo explained that this higher usage does not translate into greater amounts of total debt or financial stress.

Rather, it reflects the low credit limits given to young people and the work of rewards programmes that encourage the usage of credit cards.

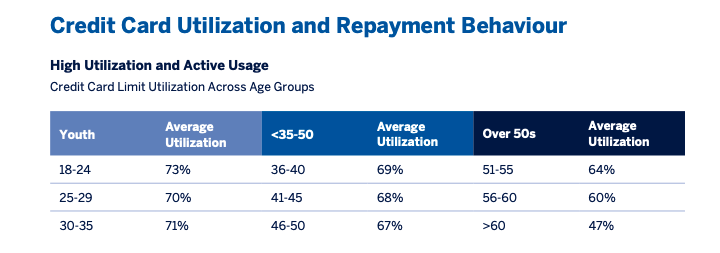

Standard Bank’s data shows that, despite the higher usage rates, the balance on individual credit cards remains stable.

This points to disciplined and more frequent repayments by young individuals. Over time, usage rates decline as incomes grow.

As incomes rise, the repayments on credit cards as a share of income decline. This is in line with previous generations and historic data.

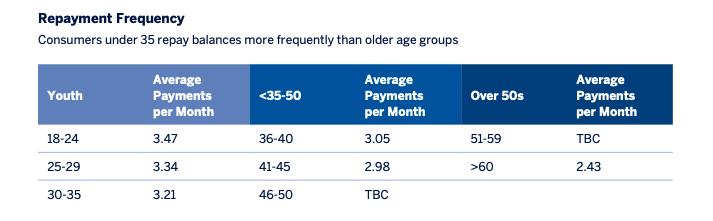

Ramugondo pointed out that young people repay their cards multiple times per month, which is a much higher frequency than older generations.

This points to the everyday use of credit cards and also the ease of banking in a digital age, where a repayment can be made instantaneously on a banking app.

Ramugondo also noted that the frequency and small-scale nature of credit card usage changes as individuals age, with debt being consolidated into larger transactions.

Comments