Capitec’s CEO does not watch its share price

Capitec has the most expensive shares of any South African company listed on the JSE, yet CEO Graham Lee said the share price is not an important metric for the company.

Instead, Capitec prefers to focus on what it can control – running a growing and client-focused company, which naturally creates shareholder value over time.

Capitec’s incredible share price growth is one of the key metrics often used to illustrate the company’s success story.

Since listing on the JSE, the bank’s share price has increased by over 300,000%. At the time of writing, it stood at just under R4,400.

Since Lee became CEO in July 2025, taking over from Capitec co-founder Gerrie Fourie, the bank’s share price has grown by over 23%.

This makes Capitec the most expensive share on the JSE, pricier than giants like Naspers, AngloGold Ashanti, and Velterra Platinum.

In an interview following the bank’s latest results for the 2026 financial year, Lee told Daily Investor that the share price is outside of the company’s control.

“If you ask me what the share price is, I would genuinely be able to tell you that I don’t know. I also didn’t know yesterday, I also didn’t know on the weekend, and I didn’t know last month,” he said.

“That’s actually really important – we don’t manage the share price, we really do focus on our clients and managing the business.”

He explained that this comes down to two reasons: the volatility of share prices and the shareholder value that is created simply by being consistent over the years.

Firstly, Lee explained that the “value” reflected in the company’s share price might appear to the outside world as changing dramatically due to forces beyond Capitec’s control.

“But we do know the value of what we create every day, and we focus on that, and when we do that consistently over the years, it will result in creating shareholder value, which does get reflected in the share price,” he said.

He explained that the “volatility and vanity” of the share price measure on any given day is not something Capitec prioritises.

The high price tag for Capitec shares has led some investors to call for a stock split, which is essentially when a company divides its stock into multiple shares, thereby lowering the price for an individual share.

However, when asked whether a stock split is something the company is considering, Lee told Daily Investor that it is not currently on the cards.

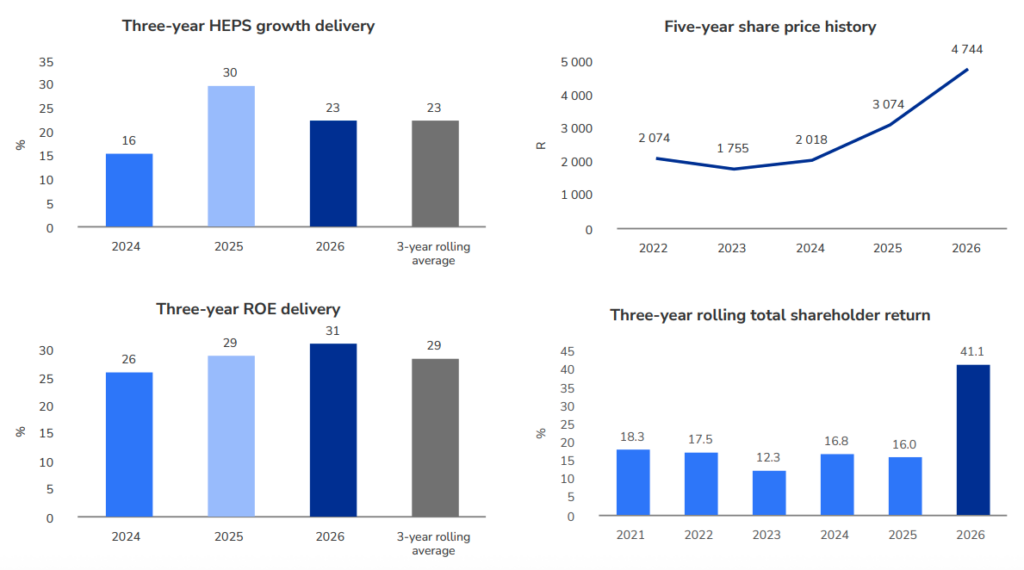

Capitec’s share price growth since listing is shown in the graph below.

From strength to strength

Capitec’s relentless focus on improving and growing its offerings has paid off handsomely for the company, and not just in its share price.

For the 2026 financial year, Capitec reported a profit of R16.84 billion and a return on equity of 31%.

Sanlam Private Wealth investment analyst Gary Davids described Capitec’s latest results as “strong and broadly reassuring”.

“Earnings growth looks well supported by diversification into non‑interest revenue, with fintech, payments and insurance continuing to provide meaningful ballast,” he said.

Capitec reported a 23% increase in headline earnings to R16.8 billion, driven by a 14% increase in net interest income and a 19% increase in non-interest income.

Davids explained that Capitec’s business banking opportunity is also contributing meaningfully, something that is expected to continue in the years ahead.

“The operating model remains capital‑efficient, returns are high, and there is clear evidence that scale and digital primacy are translating into improved unit economics,” he said.

“Importantly, credit outcomes remain within management’s guidance, and provisioning appears appropriately calibrated given portfolio growth and the stage of the cycle.”

The bank reported a credit loss ratio of 8.1% for 2026, up from 7.5% in 2025, though this was outpaced by its book growth of 9.4%.

Capitec’s Personal Banking and Business Banking segments saw their credit impairment charges on loans and advances increase by 10% and 72%, respectively.

Davids added that Capitec is now entering this phase of the cycle from a position of strong capitalisation, which provides comfort that it can absorb higher losses if conditions deteriorate.

“Capitec is less impacted by rate movements because earnings are increasingly driven by fees, usage and ecosystem scale, not by interest spreads,” he said.

This makes Capitec’s model structurally more resilient across rate cycles, provided that its credit discipline holds.

Capitec’s impressive growth metrics can be seen in the graphs below.

Comments