Old Mutual eyes South Africa’s ‘Big Four’ banks

South African equities have had a strong 2025, generating world-leading returns on the back of rising commodity prices and improving local fundamentals.

However, some sectors of the market have not felt the love, particularly companies that generate a significant share of their earnings in South Africa.

These stocks, commonly referred to as SA Inc., have been left behind by the broader rally, as investors remain cautious about the country’s lacklustre economic growth.

Examples of these stocks include South African banks and retailers, wth these indices substantially underperforming the All Share Index so far in 2025.

However, Old Mutual Investment Group’s Gustav Schulenburg expects this picture to change in the near future, with local banks being poised particularly well for strong returns.

Schulenburg explained that South African banks are exceptionally well-managed, tightly regulated, and remain well-capitalised despite elevated volatility over the past five years.

The sector is often seen as the crown jewel of the country’s economy, with its highly sophisticated and well-developed financial sector in comparison to other emerging markets.

South Africa’s ‘Big Four’ of Absa, Nedbank, Standard Bank, and FirstRand have greatly expanded their presence outside the country in recent years.

Standard Bank generates over 40% of its earnings outside of its home market, with the others looking to catch up to benefit from faster economic growth in other African economies.

However, South Africa remains the most important market for these institutions, where most of their earnings are generated, employees work, and the majority of their infrastructure is located.

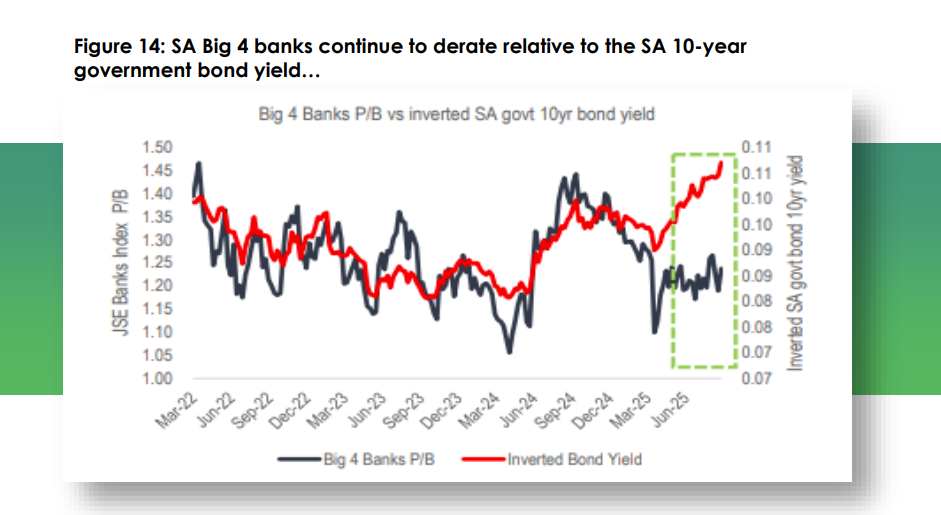

Historically, this has resulted in their performance, as measured by their price-to-book ratio, being closely correlated with the South African government 10-year bond yield.

When the yield comes down, the multiple at which the major banks trade tends to widen as financial conditions ease, and it becomes cheaper to borrow money. In times of rising yields, the opposite is true.

Schulenburg noted that this correlation has broken since the beginning of 2025, with South Africa’s bond yield coming down and the multiple at which the Big Four trades remaining flat.

The gap between these two has widened steadily throughout the year, making banks a highly attractive investment opportunity should the historical relationship be reestablished.

Schulenburg explained that the market is discounting the benefits banks may experience from a significantly lower 10-year bond yield.

This can also be seen in the dividend yield offered by these banks exceeding the returns of money market instruments.

At some point, the multiple at which the Big Four trades should stretch to bring it in line with a reduced 10-year bond yield. In the meantime, they offer investors attractive dividends.

The relationship between the bond yield and the price-to-book multiple at which the Big Four trades can be seen in the graph below, courtesy of Schulenburg and Old Mutual Investment Group. Note the bond yield is inverted on the right-hand side.

Fiscal consolidation and commodity boom

South Africa’s bond yields have come down meaningfully in 2025, making it cheaper for the government and all economic participants to borrow money.

In the case of the government, this relief is sorely needed as it spends over R1 billion a day servicing its debt burden.

The National Treasury estimates that a decline of 100 basis points in the interest rate on its debt will save the government R20 billion a year.

This silver bullet has largely come as a result of the National Treasury imposing the painful policy of fiscal consolidation and rising commodity prices.

The National Treasury’s fiscal consolidation policy entails more tax revenue being squeezed from a stagnant economy and a tight lid on government spending.

In effect, taxpayers pay more to the state in exchange for less. While painful, this has been necessary to ensure the country does not enter a debt spiral due to the government running a full budget deficit for more than 15 years in succession.

This policy is finally bearing fruit, with the government on track to post its third consecutive primary budget surplus in the current financial year.

A primary budget surplus means the government is bringing in more in tax revenue than it spends, excluding debt-servicing costs.

This means the debt burden should stabilise over time, and the government will be in a position to pay down its debt in the coming years.

The government has received a notable boost in this regard from rising commodity prices, particularly gold and platinum.

While South Africa’s participation in the historic rally of gold prices is limited due to the country having largely mined out its endowment of the mineral, the rise in PGM prices promises to boost the JSE and the government’s coffers.

Crucially, South Africa is the largest producer of PGMs, and Russia, the second-largest source, is effectively sanctioned, leaving the country in the prime position to benefit.

What remains essential, however, is how the government decides to use the potential additional revenue from the commodity boom.

Following a sustained rise in the price of PGMs in 2021, the government collected an additional R120 billion in revenue.

The key question is how these funds will be used, with analysts advising investment in infrastructure or paying down the government’s debt rather than increasing consumption and higher salaries.

Comments