South African banks opening the taps – with a big catch

Credit extension to the private sector grew strongly in September, as banks increased their lending following the steady reduction in South Africa’s interest rates.

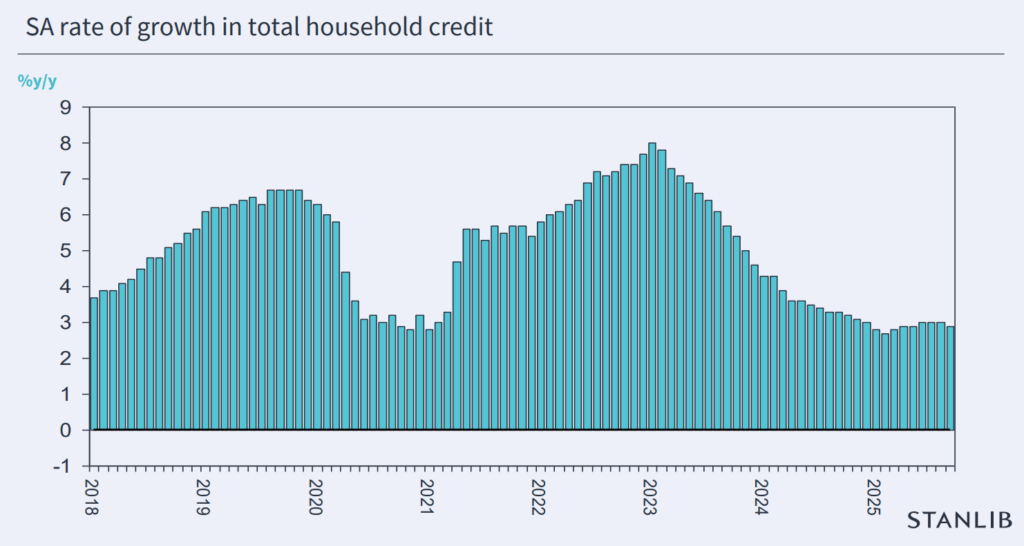

However, much of this increased credit extension is to large corporates and businesses, with household lending growth remaining subdued.

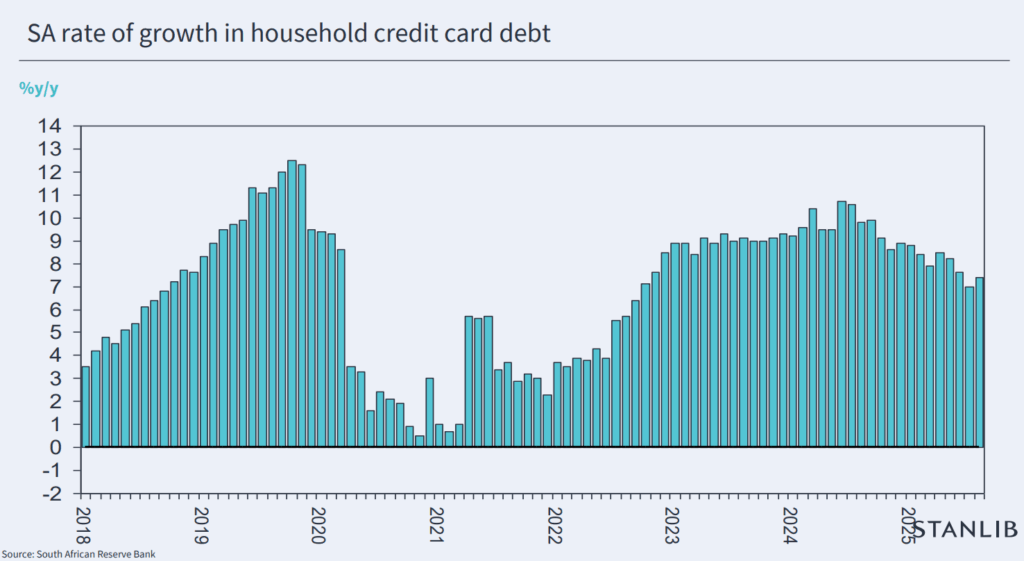

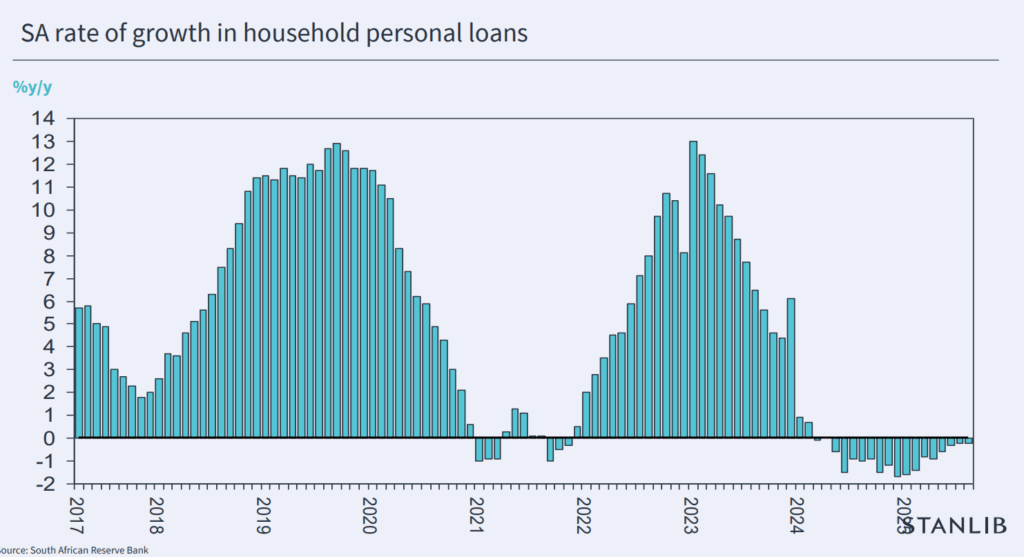

Growth in personal loans remains negative, while the rate of growth in credit card debt has continued to slow.

This indicates that banks may be pulling back from extending unsecured credit to individuals, with the relatively low debt levels of businesses making them more attractive to lenders.

Regardless, the strong growth in private sector credit extension is positive for the broader economy, indicating greater economic activity and investment from companies.

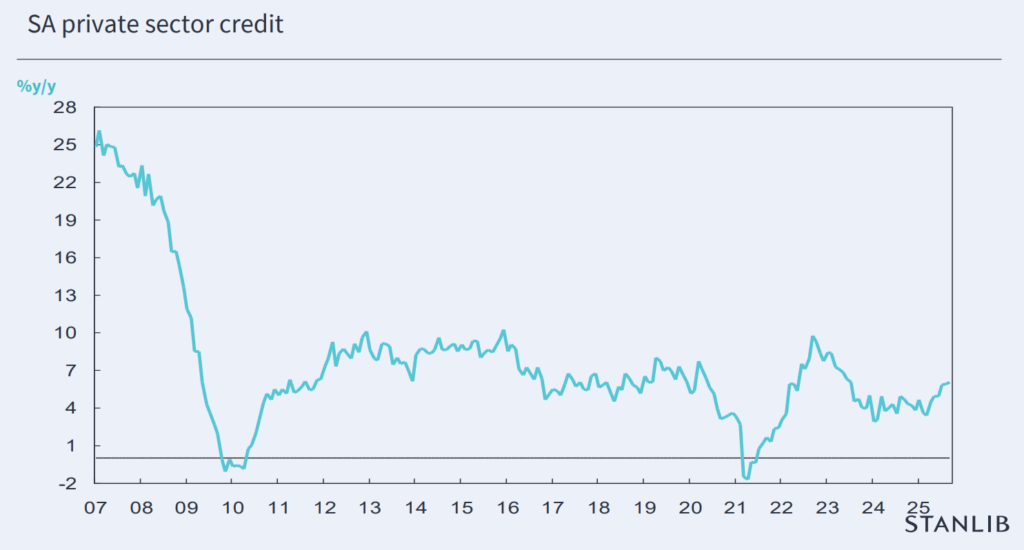

Stanlib chief economist Kevin Lings revealed that private sector credit extension rose by a substantial R70.1 billion in September, representing a 1.4% month-on-month increase.

This follows a strong August, where private sector credit extension rose by R69.6 billion, marking significant consecutive monthly increases for years.

As a result, the annual growth in private sector credit extension accelerated to 6% year-on-year in September from 5.9% in August.

This is the fastest rate of growth in credit since June 2023, Lings noted, which indicates a potential pickup in economic activity.

A breakdown of the credit extension shows that corporate credit drove most of the increase, as it rose by R64.6 billion in September.

This is in line with expectations as corporates have relatively low debt burdens and are increasingly looking to invest in substantial projects in South Africa.

S&P Global Ratings forecasted a strong increase in lending to corporates at the beginning of 2025 on the back of increased investment in alternative energy sources and backup water supply.

In contrast, household lending growth remains relatively slow with a modest R5.5 billion increase in September.

The growth in this lending has been driven largely by increases in mortgages, with credit card growth slowing and personal loans remaining in decline.

Alternative strategies

The difference between growth in corporate lending and household lending can also reflect the alternative strategies of various banks.

South Africa’s traditional Big Four banks – Absa, Standard Bank, Nedbank, and FirstRand – have substantial corporate and investment banking businesses.

In most cases, this division brings in the largest share of headline earnings for these institutions, as it is a highly lucrative subsector of banking.

The credit-loss ratio within corporate and investment banking is also extremely low compared to personal lending, making it more attractive to banks.

Lending in this sphere also tends to outweigh household credit extension purely due to scale, with corporates requiring much more significant financing compared to individual products.

Lending to this area has been driven largely by investments in renewable energy projects and will be fuelled by private investment in South Africa’s transmission grid and logistics infrastructure in the coming years.

These banks also have large personal and private banking businesses, but they have proven to be stricter in extending credit in this sphere as household finances come under pressure.

In contrast, other banks, such as Capitec, Discovery Bank, and TymeBank, which are heavily focused on retail banking, are rapidly growing their lending to households and individuals.

Thus, while all South African banks are broadly in an expansionary phase, the differentiation in strategies is expected to be seen in more stark terms.

FNB CEO Harry Kellan explained that the bank is stepping up lending more aggressively in South Africa, betting on its healthier balance sheet and improved consumer financial health.

“We are expecting better growth rates of advances in the next 12 months because impairments have stabilised,” Kellan told Bloomberg.

“While the strain in consumers continues, the affordability for some individuals has improved, which means that our lending capacity has increased.”

FNB was relatively cautious in 2020 and the years that followed, while interest rates were at multi-year lows to contain its credit loss ratio and ensure the bank was in a position to pick up lending in future.

The strategy kept the lender’s credit loss ratio — bad loans as a share of total lending — below the top of its 80-to-110 basis-point target, while rivals Absa and Nedbank breached their ceilings in 2023. Absa only pulled its ratio back within target by June this year.

Capitec is also relatively more aggressive in its lending to clients, growing its personal banking and business banking loan book strongly over the past financial year.

Standard Bank has increased its lending, but this is largely driven by the bank’s substantial corporate and investment banking division.

This division has been the largest funder of renewable energy projects and infrastructure in South Africa and the wider continent, focusing its strategy of focusing on long-term trends.

Comments