The South African bank gunning for Capitec with 5,000 new clients a day

OM Bank is currently onboarding around 5,000 customers per day, with the new challenger having 140,000 active customers just three months after its soft launch.

This marks a strong start for the bank, which has not undergone a full public launch as yet, with that set to occur in November 2025.

Old Mutual revealed this as part of its 2025 Capital Markets Day, where CEO Jurie Strydom outlined how he plans to revive the insurer.

One of the key aspects of his plan is to expand Old Mutual’s banking and lending proposition through its new bank.

Strydom said it was natural for Old Mutual to launch a standalone banking offering given its immense scale and the company’s existing lending operations.

Crucially, the bank also gives the insurer the ability to cross-sell insurance and investment products through a more interactive client base.

Old Mutual estimates that a banking app will bring it around 24 times more interactions per client per year, giving it a significant new distribution channel to customers for insurance and investment products.

Currently, it is focused on leveraging its existing Money Account client base and incorporating the Old Mutual Finance business.

These two operations are sizeable in their own right and give OM Bank a significant headstart over an entity that would have launched from scratch.

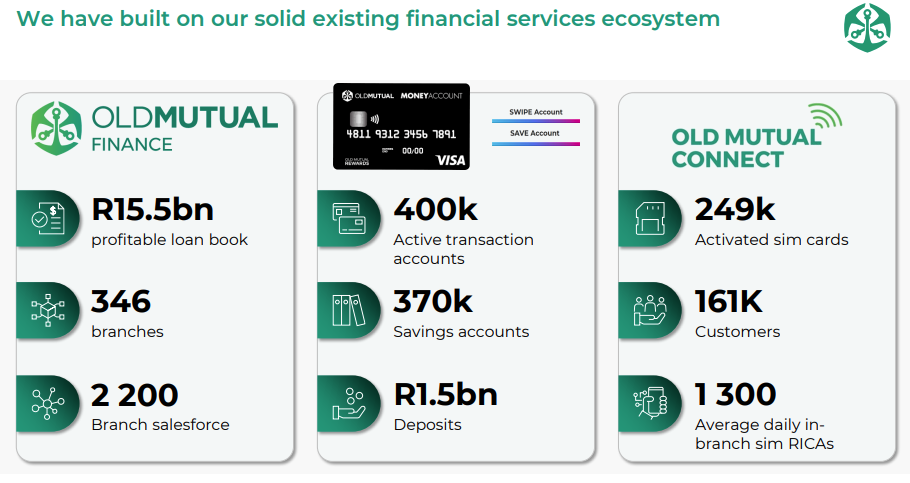

Old Mutual Finance sits with a R15.5 billion loan book, which it says is profitable, and a strong branch network with 346 branches and 2,200 staff.

The Money Account offering, administered by Bidvest Bank, has around 400,000 active transaction accounts and 370,000 savings accounts. It sits with R1.5 billion in deposits.

These two existing ‘banking’ businesses will be coupled with Old Mutual Connect, the insurer’s Mobile Virtual Network Operator.

This brings around 161,000 customers with 249,000 activated SIM cards into the fold. Old Mutual said it averages 1,300 daily in-branch SIM card RICAs.

The combination of these offerings under the bank gives it immense scale relatively quickly and a physical branch network that does not require significant investment to build out.

These substantial businesses that have been folded into OM Bank can be seen in the graphic below.

Scaling to profitability

In his presentation, taking investors and analysts on a deep dive of OM Bank, its CEO Clarence Nethengwe explained how it will become profitable.

Old Mutual currently expects the bank to run at an annual loss of between R1.1 billion and R1.3 billion until the 2028 financial year.

In that year, OM Bank is set to become profitable if it can meet its ambitious client acquisition goals of attaining 2.8 million customers by then.

Currently, Nethengwe explained that the bank is onboarding around 5,000 customers a day from its existing Money Account clients and a limited public launch.

As of 28 October, OM Bank has 140,000 active customers, up from 5,700 in July and 17,000 when it conducted a limited soft launch.

Nethengwe explained that the bank expects to pick up a further 500,000 Money Account clients and attract one million existing Old Mutual clients to the bank.

This will result in OM Bank needing to attract 1.1 million clients that are entirely new to the Old Mutual Group.

Nethengwe also further explained the bank’s collision course with Capitec, which dominates low-cost banking in South Africa.

OM Bank is targeting the 7 million customers sitting in its Mass and Foundation cluster, many of whom have products with the insurer, such as funeral insurance or life insurance.

These individuals typically earn between R8,000 and R80,000 per month – a market segment dominated by Capitec and filled with smaller fintechs.

This competition with Capitec is as much about growing Old Mutual’s presence in banking as it is about protecting its existing business.

Research from Swiss Re, one of the world’s largest reinsurance companies, shows that Capitec may take up to 36% of all new funeral insurance sales.

This is a significant share that poses a major threat to Old Mutual’s insurance business. If Capitec can replicate this success with other insurance products, it can take a substantial chunk of Old Mutual’s Mass and Foundation Cluster.

As a result, the launch of OM Bank is a way to compete on equal footing against this threat by using its banking offering to cross-sell Old Mutual’s insurance products to a wider customer base.

The graph below outlines OM Bank’s exisitng client growth and the forecasted growth needed to break even in 2028.

Comments