One group of South Africans face a serious debt problem

Between high debt levels, low incomes, and limited credit histories, South Africa’s youth are facing a challenging economic environment.

This was revealed by Eighty20’s National Segmentation, which investigated the credit behaviour of South African youths aged 18-24.

South Africans aged 24 and younger make up about 44.5% of the country’s population. Among the 6.7 million young people aged 18 to 24, roughly 1 million are credit-active out of around 20 million credit-active individuals nationally.

“They’ve got a lot going against them,” Andrew Fulton, Director at Eighty20, pointed out on the Kaya Bid podcast.

“Their average monthly incomes are about R3,400 a month, which is half the national average.” Additionally, he said that about half of them defaulted on their loans if they had one.

Overall, this age group holds about R10 billion in total debt, only about 5% of the national credit by value. However, R1.1 billion of that is overdue, an arrears rate of more than 10%. This shows how many are struggling to repay.

This group is also facing high rates of unemployment. According to the latest Quarterly Labour Force Survey (QLFS) released by Statistics South Africa (Stats SA) for Q1 2025, the 15-24 age group faces the highest barriers to entering the workforce.

In Q1 2015, this youth group had an unemployment rate of 50.3%. A decade later, it has shot up to 62.4%.

“The challenges facing young South Africans in the employment space are not new, but they are trending negatively in many cases,” Stats SA said. “Over the past ten years, youth unemployment has remained persistently high.”

With unemployment being so high, many people, even those employed full-time, are turning to side hustles just to keep up since income isn’t keeping pace with inflation.

A BrandMap survey, which focuses on households earning more than R10,000 per month, found that in 2021, 55% reported having no side hustle.

By 2024, that dropped to 49%. This indicates that an increasing number of people are starting side businesses or taking on second jobs in their field.

From 2021 to 2024, the percentage of people running a small business or working a second job grew by 50%. This mirrors global trends. For example, about half of millennials and 46% of Gen Z internationally now report having side hustles.

Thin file clients

Eighty20 specifically examined “thin file” clients, which are individuals who have applied for credit for the first time within the past three months.

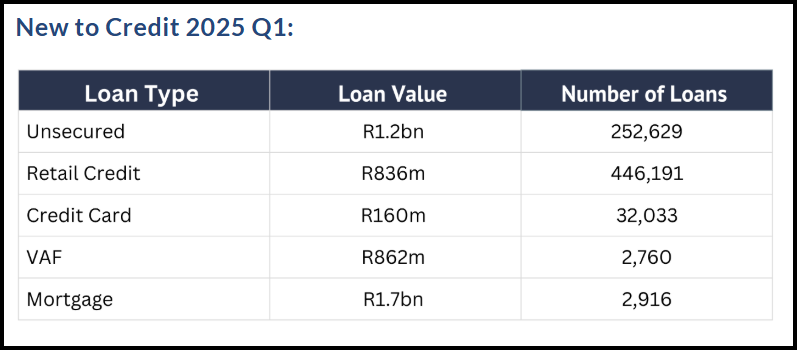

It found that the number of new-to-credit individuals in the first quarter of 2025 was just over 700,000. This is a 27% increase from the previous year, although this number varies from quarter to quarter.

There were more than a million new to credit in the second and third quarters of 2024 as inflation eased and the first repo cuts came in. The total debt these new-to-credit individuals took in 2025 Q1 was R4.8 billion, a 5.9% decrease from Q4 2024.

Fulton said that around 20% of South Africans under 24 are considered “thin file” clients. Over the past three months, between 150,000 and 200,000 young people entered the credit system.

There were some interesting trends in terms of who these applicants were. Nearly all (98%) thin file clients earn less than R20,000 monthly personal income. More than a quarter of all credit-active earn more than R20,000 per month.

While three-quarters of credit-active individuals are over 45, nearly half of thin-file clients in Q1 2025 were under the age of 45.

Monthly, between a half and two-thirds of loans opened by first-time credit applicants are retail credit, with about a third being personal loans. Together, these products make up less than 50% of all new loans by value.

This trend was similar for 18-24-year-old thin file clients. In Q1 2025, about 85% of this group started with retail credit. According to Fulton, there are two reasons for this.

First, they are likely being encouraged to open store cards to establish credit before applying for other types of loans. Second, they may be tempted to use retail credit to buy new clothing simply to get instant gratification.

During Q1 2025, 13% of South Africa’s youth also took out credit in the form of unsecured personal loans and 9% via credit cards. Very little of this is asset-building debt.

In general, Fulton pointed out that the country’s youth are using credit in a concerning way. However, young consumers are getting into unsecured debt, not because they’re irresponsible, but because of their stage in life and lack of credit history.

Given how many young people’s debts are overdue, this credit usage does not lead to long-term stability like home ownership or business investment.

Comments