South Africa faces serious economic crisis

South Africa is heading for serious financial trouble. The government’s fiscal deficit is set to widen in the coming years, threatening its plans to stabilise its substantial debt burden.

This is mainly due to rising debt-servicing costs, which are set to amount to R424.9 billion in the current financial year, and the government’s significant ‘social wage’.

The social wage, which includes social grants, education, healthcare, and housing, makes up 61% of total non-interest spending.

As a result, the National Treasury has consistently pushed back the year in which it expects the government to run a full budget surplus.

Currently, the government runs a primary budget surplus of around 0.5% of GDP, which excludes debt-servicing costs. Its full budget deficit is around 5% of GDP or R374.7 billion.

While running a budget deficit is not a bad thing by itself, the government has consistently run deficits and racked up a huge debt burden of 76% of GDP.

With the country’s high interest rates resulting in elevated debt-servicing costs, spending on servicing this debt is now beginning to crowd out expenditure in other areas of the economy.

For example, in the country’s Budget for the 2025/26 financial year, the government is set to spend more on interest payments than economic development.

Debt-servicing costs will remain the fastest-growing expenditure item in the budget, growing by an average annual rate of 7.1% for the next three years.

This will increase debt-servicing costs to R478.6 billion in 2027/28, translating into R1.3 billion a day. It will also mean the government will spend more on interest payments than on social grants and healthcare.

Worryingly, the South African government’s interest rate on its debt is higher than the country’s economic growth, even in nominal terms.

The government borrows at an interest rate of around 9%, while nominal economic growth hovers around 5%.

Tax revenue will grow more or less in line with nominal economic growth over time, assuming a steady tax-to-GDP ratio.

This gap between interest rates and growth, sometimes expressed as r>g by economists, renders borrowing unsustainable since debt compounds faster than the income needed to service it.

National Treasury’s plan

The government has planned to tackle this through enhanced tax collection by capacitating SARS and fiscal consolidation, to run a primary budget surplus.

A primary budget surplus means that, in the long term, government debt should stabilise and begin to come down as money is freed up to pay down the principal owed.

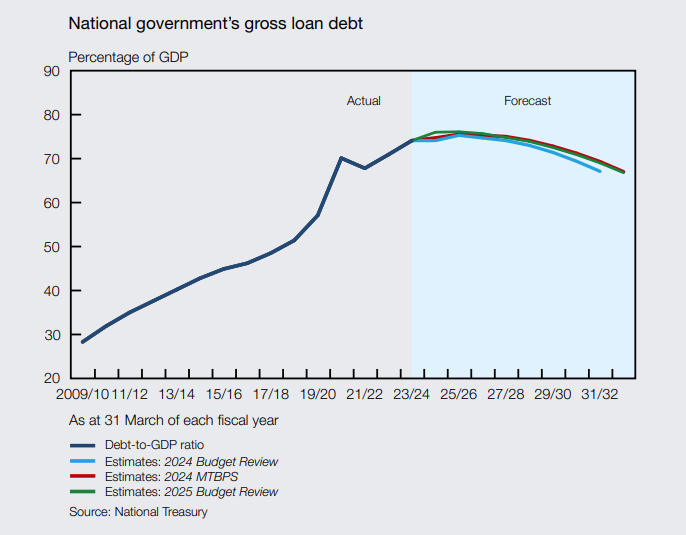

The National Treasury estimates that government debt will stabilise at 76.2% of GDP in 2025/26, higher than previously forecast.

“As debt stabilises, a growing primary surplus will enable the government to reduce debt-service costs as a proportion of revenue,” Finance Minister Enoch Godongwana said during his Budget Speech.

“Some of these savings will be used to build up fiscal buffers that we need as protection against future economic shocks.”

While this is all positive, it will take years before South Africa begins to see the benefit of a primary budget surplus, particularly one so small.

In its latest Quarterly Bulletin, the Reserve Bank analysed the National Treasury’s data regarding its forecasts for the government’s fiscal balances.

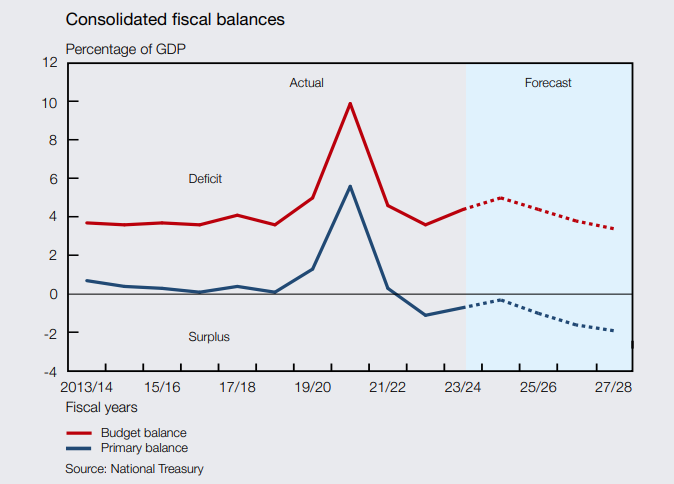

The consolidated budget deficit has been revised higher to 5.0% of GDP in fiscal 2024/25 from the projected 4.5% in the 2024 Budget.

However, the consolidated budget deficit is expected to narrow to 3.5% in fiscal 2027/28, with consolidated non-interest expenditure expected to increase at an annual average rate of only 0.8% in real terms over the next three years.

In addition, the government anticipates a primary surplus, where revenue exceeds non-interest expenditure, of 0.5% of GDP in fiscal 2024/25, widening to 2.0% of GDP in fiscal 2027/28.

The main budget deficit is also expected to continue narrowing over the medium term, from 4.4% of GDP in fiscal 2025/26 to 3.3% in fiscal 2027/28.

In fiscal 2025/26, the gross borrowing requirement will be financed through a combination of domestic short and long-term debt and foreign debt.

The national government’s total gross loan debt is expected to increase from R5.7 trillion (76.1% of GDP) in fiscal 2024/25 to R6.8 trillion (75.1% of GDP) in fiscal 2027/28.

Gross loan debt is now expected to stabilise at 76.2% of GDP in fiscal 2025/26, higher than the 75.3% projected in the 2024 Budget.

The Reserve Bank warned that debt-servicing costs may rise further due to this increased debt load, elevated interest rates, and a weaker exchange rate.

Over the MTEF period, the government expects to spend more on debt-service costs than on health, basic education and social development.

Debt-servicing costs are projected to rise from R389.6 billion in fiscal 2024/25 to R478.6 billion in fiscal 2027/28, but, as a percentage of revenue, are projected to stabilise at 21.7% in fiscal 2024/25.

Comments