Bad news for South African businesses

South Africa’s economic recovery is proving fragile, with businesses being unable to manage their debt obligations effectively and unwilling to invest in growth.

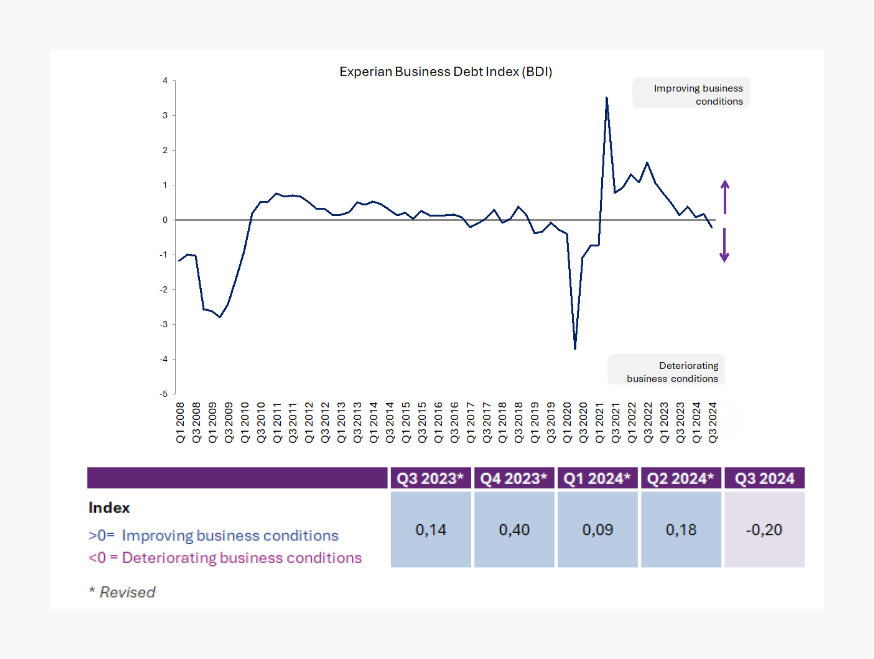

This was revealed in the Experian Business Debt Index (BDI) for the third quarter of 2024, which showed a sharp downturn from the previous period’s modest improvement.

The BDI slipped to -0.20 from a positive 0.18 in Q2, reflecting the pressing impact of unforeseen agricultural setbacks and persistent logistical hurdles on local businesses.

Experian’s index measures business conditions in South Africa, considering both businesses’ ability to pay their outstanding suppliers or creditors on time and several macroeconomic indicators.

The decline comes despite several positive factors, such as the end of load-shedding, the new Government of National Unity (GNU), and declining lower interest rates, which were initially expected to boost the BDI.

“While the Q2 improvements offered a glimmer of hope, the sharp reversal in Q3 highlights the fragility of the current economic recovery,” said the head of commercial strategy and innovation at Experian, Jaco van Jaarsveldt.

“The unforeseen challenges faced by the agricultural sector, coupled with persistent logistical bottlenecks, have significantly impacted businesses’ ability to manage their debt obligations effectively.”

In particular, small to medium enterprises have been hit the hardest, with them now facing their highest debt stress levels since 2022.

This is concerning for the local economy as these businesses provide most of the employment in South Africa and have long been touted as having the potential to drive the country’s economic growth.

A key driver of the BDI decline was the substantial contraction in agricultural GDP (-29% quarter-on-quarter), attributed to a combination of drought, floods and livestock diseases.

This contraction had a ripple effect across the economy, exacerbating business debt conditions.

Furthermore, a sharp decline in producer price inflation, which outpaced consumer price inflation, eroded profit margins, adding to the financial stress businesses face.

Additionally, persistent logistical challenges in rail transport and port operations strained the transport sector, contributing to the overall economic slowdown.

These factors appear to have fostered a more cautious approach among businesses, leading to a decline in timely debt repayments.

In contrast, the electricity and construction sectors recorded improvements, largely due to a rebound from previously depressed levels caused by load-shedding and a lack of investment.

Despite the Q3 setback, Experian said there are reasons for cautious optimism in Q4 and beyond.

The continued absence of load-shedding, ongoing government efforts to address economic challenges and the potential for further interest rate cuts could contribute to improved business conditions.

However, persistent agricultural challenges, delays in port infrastructure improvements and global economic uncertainties limit the potential upside.

“South Africa’s long-term prospects depend on addressing these challenges through strategic structural reforms,” Van Jaarsveldt said.

Key areas for reform include improving logistical efficiency in rail transport and ports, which are vital for boosting trade and productivity.

More recently, water shortages have become a significant challenge which needs to be addressed through better infrastructure management to sustain agricultural output and support industrial activities.

However, there are plenty of reasons to be positive about the South African economy in the near future, with significant progress being made regarding structural reforms.

Economists surveyed by Bloomberg expect the economy to grow by 1.7% in 2025 compared to a mere 0.7% in 2024.

While this is an improvement, it merely indicated a period of stabilisation rather than deterioration, the head of macroeconomic research at Standard Bank South Africa, Dr Elna Moolman, said.

“What is important is that we are moving in the right direction, and this is not just a cyclical improvement or a reaction to interest rate cuts,” Moolman explained.

Moolman said it would be important to see the private sector’s response to the improvement in electricity supply and the formation of the GNU.

The reaction is expected to be positive, with many companies finally using the cash on their balance sheets to invest in growth rather than subsistence.

“This year, we will see how private sector companies actually respond to an improved political environment,” Moolman said.

“We have seen a slight uptick in business confidence and view in fixed investment improve. However, this year, we will see if they actually invest in expansion and add productive capacity or if it will be more of just treading water.”

She said Standard Bank’s research expects economic growth to be above 2% next year and then gradually improve further after that.

Comments