The rand is weaker than it seems

The rand continues to hold its own against the dollar, with it edging towards R17.20 to the US dollar despite elevated geopolitical tensions and uncertainty.

Typically, in this environment, the rand would weaken significantly versus the dollar as investors flock towards safer assets and out of emerging markets, such as South Africa.

This has been the case so far in 2025, but the dollar has weakened substantially while other major currencies have strengthened.

Investec chief economist Annabel Bishop explained that this indicates investors are no longer treating US Treasuries as the safe-haven asset they once were due to America’s deteriorating financial health.

Bishop said that the rand has not strengthened on its own and much of its performance against the dollar is due to the greenback’s weakness, not the rand’s strength.

This can be seen in how the local currency has fared against other major currencies and in how much the dollar has weakened in 2025.

The US dollar has weakened by 9.7% since the start of 2025, but the rand is only 8.3% stronger against the greenback – indicating that the local currency is not as strong as it seems.

America’s greenback has seen marked weakness this year on concerns around US economic growth and the Trump administration’s preference for a weaker dollar.

Expectations of US interest rate cuts from the Federal Reserve have also weighed on the dollar, with more cuts expected this year and next.

In contrast, the rand has weakened against the euro by 3.6% since the beginning of the year, pointing to the overall story being one of dollar weakness and not rand strength.

Investors have pivoted slightly towards European assets and away from the US market due to concerns about America’s financial health and increased spending from major economies in Europe, particularly Germany.

The rand has strengthened slightly against the British pound as the United Kingdom experiences its own financial troubles.

However, on average, the rand is weaker against the pound across 2025 so far, with the average exchange rate being R23.84 to the pound.

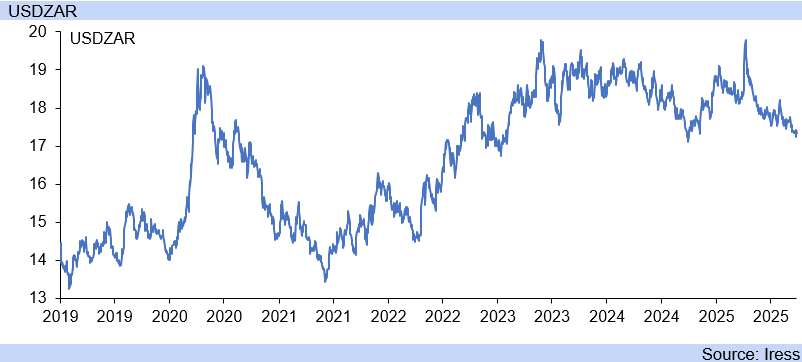

The rand’s movements versus the dollar over the past six years can be seen in the graph below, courtesy of Annabel Bishop.

Deal or no deal

Bishop explained further that local developments are far outweighed by moves in global currencies in determining the value of the rand.

This even applies to developments regarding South Africa’s potential trade deal with the United States, which has barely impacted the currency’s value compared to the start of the year.

The rand has not reacted significantly to positive or negative developments, with it being more sensitive to US-China relations, commodity demand, and global uncertainty.

South Africa’s currency is also significantly impacted by expected interest rate cuts in the United States, which have impacted the attractiveness of fixed-income investments.

As the Federal Reserve cuts interest rates and the Reserve Bank takes a more cautious stance, South African fixed-income investments become relatively more attractive on a risk-adjusted basis.

This attracts more capital towards these investments, particularly government bonds, and increases demand for the rand, boosting its value.

However, this script may flip as the Federal Reserve’s models indicate only one more cut to interest rates in the US as its economy remains stronger than expected.

Last week, the US saw its manufacturing PMI remaining in positive territory, along with its services and composite PMI, while its second-quarter GDP growth surprised on the upside at 3.8%.

Furthermore, preliminary figures show that in August, durable goods orders lifted 2.9% from July, versus an expected contraction. Personal spending and income were also higher for the month than expected.

The stronger-than-expected data on the US economy have seen financial market expectations now only factor in one further 25 basis points cut in US interest rates this year, from previous expectations for two cuts for the rest of this year.

This may result in the dollar strengthening slightly against the rand, while local headwinds such as a widening current account deficit may weaken the South African currency.

South Africa’s deteriorating logistics infrastructure, pressure from United States tariffs, and increased demand for imports have weakened the country’s terms of trade.

While this weakening is not at crisis levels yet, South Africa’s current account balance is heading in the wrong direction.

With the country’s current account deficit widening to just over 1% of GDP, pressure is beginning to mount on the rand.

Stanlib chief economist Kevin Lings explained that South Africa’s current account deficit is at an acceptable level at around 1% of GDP, but is trending in the wrong direction.

“Overall, you would say that our trade balance is manageable, but is moving in the wrong direction,” Lings told The Business Show.

A current account deficit weakens a country’s currency by increasing its supply and foreign currency demand, leading to depreciation of a local currency, such as the rand.

This happens because a deficit implies a country is spending more on foreign goods and services than it earns, requiring it to supply more of its own currency to pay for imports while receiving less foreign currency for exports.

The increased supply of domestic currency and higher demand for foreign currency in the forex market drive the domestic currency’s value down.

“It is not putting us under enormous pressure as yet, because you can see the rand is holding on,” Lings said.

“If it becomes a big problem, then you will see the rand normally weaken. The rand has not done that yet.”

However, Lings said the country’s widening current account deficit is something South Africa needs to pay attention to.

“We are managing, but it is something that we need to pay attention to because it can get quite a bit worse,” he said.

Comments